As a parent, I remember this question well from days past. This time, however, it’s being asked by those of us with money invested in the global stock and bond markets.

As a parent, I remember this question well from days past. This time, however, it’s being asked by those of us with money invested in the global stock and bond markets.

All of us are following a life path that includes stops along the way. Some stops we choose to make and others are forced on us. Some of them are in good places and others not so good places. These comments talk about a bad one on the horizon and how your life might be better if you don’t have to stop.

Sometime soon, most likely in the next three 3 years, many of us will hit a road block. With that in mind, what follows is designed to help the reader gain a better understanding about how to have money positioned before that happens. This is particularly important if you are soon to be, or are already, retired.

In retirement, your investment focus will shift away from the accumulation of money and focus instead on the distribution of money. That’s not to say your money will no longer accumulate, but the emphasis will change. This is because instead of you working FOR money, money now has to work for YOU.

None of us individually has any control over the markets. What we do have is control over where and how our money is working for us. For almost everyone, the rules that define successful accumulation are different from the rules that define successful distribution.

Two primary drivers that define success in either phase are the stock market and the bond market, which is driven by interest rates. Knowing more about why this is relevant is in your best interest. You will also find it’s in your best interest to avoid the coming road block if you can.

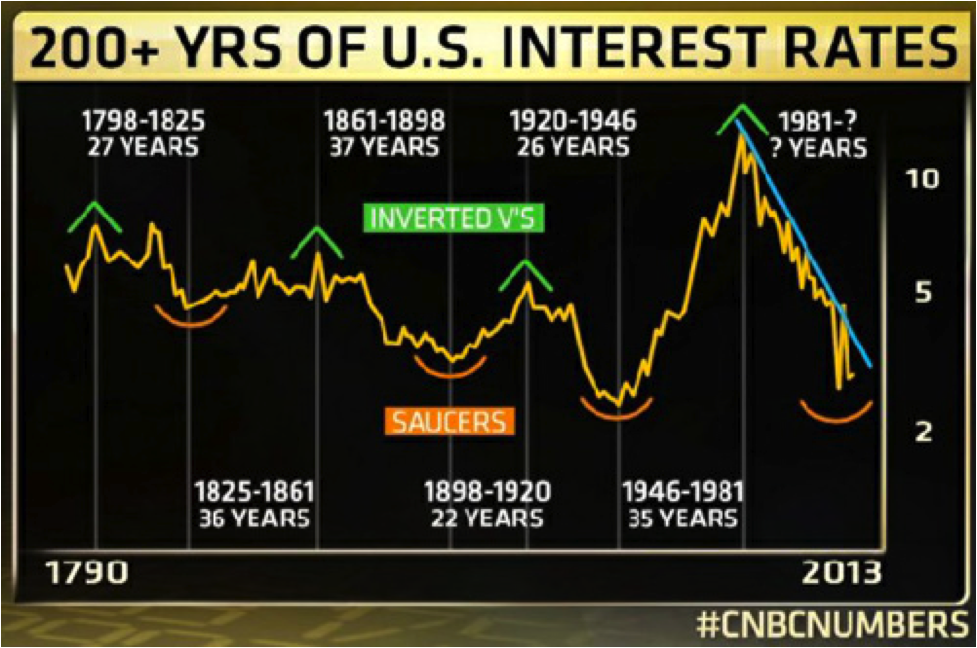

Let’s first look at interest rates. Following this paragraph is a chart that shows the general level of interest rates in the U.S. over the past 222 years. In that entire time, you see four high points in green and low points in orange. The time span from high points to low points has been 27 years, 37 years and 26 years. The last high point was in 1981, 34 years ago. What this suggests to me is that with current interest rates near zero, an upturn in rates is going to happen. How soon is up for debate, but inevitable.

When interest rates rise, the effect on bond values is negative. No one is going to pay you as much for a bond that yields 4%, if with the same money they can buy a bond that yields 5%. This is a fundamental law of finance. Before the shift happens, you should be out of bonds and into cash or into tactical approaches that help you avoid losses.

When interest rates rise, the effect on bond values is negative. No one is going to pay you as much for a bond that yields 4%, if with the same money they can buy a bond that yields 5%. This is a fundamental law of finance. Before the shift happens, you should be out of bonds and into cash or into tactical approaches that help you avoid losses.

Let’s now look at the stock market. Instead of individual stocks, I’m going to focus on the S&P500 Index, widely regarded as representing the entire US stock market. It includes the 500 largest capitalized companies in the US, many of whom sell globally, so their performance to some degree reflects what is happening across the planet.

The next chart reflects the closing price of the S&P500 on every given trading day over the past 40 years. These years largely reflect how the dollars you had invested in the stock market performed as it accumulated. Your goal at the time was to grow your pile of money as large as reasonably possible.

Retirement was down the road, and if a road block happened, it didn’t matter so much. What you heard everywhere was “buy and hold” or “hang in there”. But now the rules are different and the big question you must ask is “When Will The Next Downturn Happen?”. Or perhaps “Are We There Yet?”.

From 1975 -1982, the rise was imperceptible. Then it started upward and in spite of what happened in 1987, it was a lot of fun. Then came the internet bubble that burst in early 2000 and we all experienced the pain associated with large declines in our account values.

From 1975 -1982, the rise was imperceptible. Then it started upward and in spite of what happened in 1987, it was a lot of fun. Then came the internet bubble that burst in early 2000 and we all experienced the pain associated with large declines in our account values.

Next came the mortgage bubble that burst in 2008-2009. Again there was a lot of pain and some of us are still recovering from that episode. For the past 3 years we’ve been watching what appears to be an inexorable climb up above previous historic highs.

I try to avoid promoting a sense of fear. However, there seems to be an inevitability about the fact that sometime, most likely in the next few years, there is going to be another bubble. Again there will be widespread pain and fear and gloom across the country, if not the entire planet. Perhaps a better question to ask is “Are You Ready For It?” Or maybe “When it Happens, Will You Be Able to Sleep At Night?”

My point is to cause you to evaluate or re-evaluate what you are doing now and consider options that will eliminate some of the pain that is sure to come, and to consider options that might even cause your accounts to grow.

While all of this is speculative, it is based on historical experience. And unless you plan to be dead in a few months, how all this plays out could dramatically influence your peace of mind and financial freedom in the years to come. Not to mention the financial freedom of those you leave behind.

All of us have different pain thresholds. The more money we have compared to our accepted standard of living, the less likely the pain. What you choose to do with your life in retirement, however, is up to you.

If you take appropriate steps to protect yourself, then chances of a succesful retirement from a financial perspective are better. Living a life free from fear about your financial future is possible.

It’s up to you what you do. But I encourage you to believe acting sooner rather than later will be in your best interest.

(The charts were found at finance.yahoo.com)

by Tony Kendzior, CLU, ChFC / October 1, 2014