Tony’s Comments: What is often overlooked by those writing about the impending doom of the stock market is the age of the reader. What I mean by this is that if you are trying to accumulate money for your eventual retirement, and you have 20 or 30 years between now and then, much of what is going on now is irrelevant.

However, if you are likely to retire in the next few years, or are already retired, then it’s a very different story. Once you turn off the ‘working for money’ switch and turn on the ‘money is working for you’ switch, an end to the current bull market is very relevant.

Many people can expect to live 25 years or more in retirement. And for each of those years, one way or another you’ve going to have bills to pay. And that money needs to come from somewhere. No one is going to suddenly show up at your front door and hand you the keys to the kingdom.

August 18, 2018 by Lance Roberts

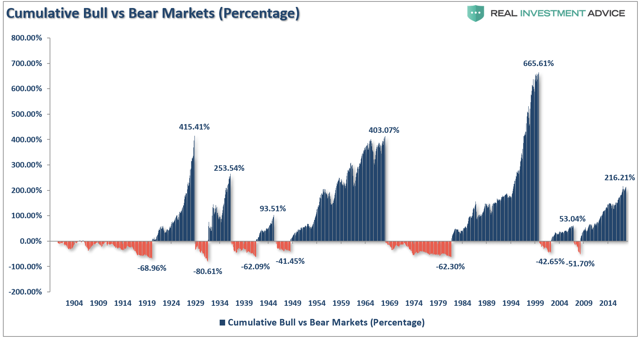

Depending on how you measure beginnings and endings, or what constitutes a bear market or the beginning of a bull market, makes the statement a bit subjective. However, there is little argument the current bull market has had an exceptionally long life-span.

But rather than a “siren’s song” luring investors into the market, maybe it should serve as a warning.

“Record levels” of anything are “records for a reason.”

It should be remembered that when records are broken that was the point where previous limits were reached. Also, just as in horse racing, sprinting or car races, the difference between an old record and a new one are often measured in fractions of a second.

Therefore, when a “record level” is reached, it is NOT THE BEGINNING, but rather an indication of the PEAK of a cycle. Records, while they are often broken, are often only breached by a small amount, rather than a great stretch. While the media has focused on record low unemployment, record stock market levels, and record confidence as signs of an ongoing economic recovery, history suggests caution. For investors, everything is always at its best at the end of a cycle rather than the beginning.

The chart below has been floating around the “web” in several forms as “evidence” that investors should just stay invested at all times and not worry about the downturns. When taken at “face value,” it certainly appears to be the case. (The chart is based up Shiller’s monthly data and is inflation-adjusted total returns.)

The problem is the entire chart is incredibly deceptive.

More importantly, for those saving and investing for their retirement, it’s dangerous.

Here is why.

The first problem is the most obvious, and a topic I have addressed many times in past missives, you must worry about corrections.

“Most investors don’t start seriously saving for retirement until they are in their mid-40s. This is because by the time they graduate college, land a job, get married, have kids and send them off to college, a real push toward saving for retirement is tough to do as incomes, while growing, haven’t reached their peak. This leaves most individuals with just 20 to 25 productive work years before retirement age to achieve investment goals.

This is where the problem is. There are periods in history, where returns over a 20-year period have been close to zero or even negative.”

Currently, we are in one of those periods.

CONTINUE READING HERE…