My Comments: You’ve read my earlier comments about whether the world we now live in is a different world. The details have changed, but the fundamentals have not. The following article will cause you to think twice if have not made plans for your money to be protected going forward.

My Comments: You’ve read my earlier comments about whether the world we now live in is a different world. The details have changed, but the fundamentals have not. The following article will cause you to think twice if have not made plans for your money to be protected going forward.

Charlie Bilello, Pension Partners, Mar. 18, 2015

Summary

• The last six years have been one of the strongest periods in history for U.S. equities.

• Investors need to lower their expectations for the next six years.

• This is quite possibly the worst starting point (looking ahead six years) for a 60/40 portfolio in history.

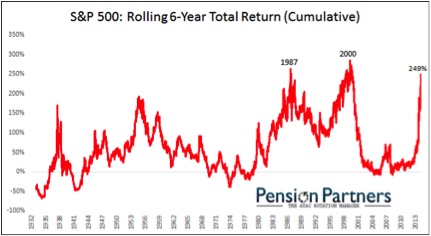

The Bull Market turned six last week and what an incredible six years it has been. From the depths of despair in March 2009, the S&P 500 (NYSEARCA:SPY) has more than tripled in one of the greatest six year bull market runs in history.

The Next 6 Years

There is a growing contingent of market participants today that seem to believe 20% annualized returns are the “new normal,” and the next six years will mirror the last. The crux of their argument is as follows: with central banks around the world engaging in unprecedented easing, there is no limit to how high a multiple the S&P 500 can fetch. In short, the narrative is that in the new central bank era, historical norms can be safely discarded as trees can grow to the sky.

While anything is possible, we should also consider a world where trees do not grow to the sky and mean reversion still exists. In that world, the “old normal,” a repeat performance is unlikely for the following reasons:

1) The average annualized return for the S&P 500 since 1928 is 9.3%. To expect the market to more than double this return for another six years is to expect the greatest bubble in the history of markets, far surpassing the dot-com bubble that peaked in 2000.

2) The long-term price-to-earnings ratio (CAPE or Shiller P/E) of 28 is now higher than all prior periods since 1871 with the exception of 1929 and the dot-com bubble which peaked in 2000.

3) While a terrible short-term predictor, there is a strong inverse relationship between longer-term returns and beginning price-to-earnings ratios, particularly at extremes. The worst decile of Shiller P/E values in the past (levels >26.3) have shown the worst average forward returns at 1.7%.

4) The gains of the past six years have not been lost on investors, who are about as bullish as they have ever been. The 45% spread between bulls and bears today stands in stark contrast to the -20% spread six years ago. The strongest gains in equity markets are built on a wall of worry and there is no such wall to speak of anymore.

While these factors may certainly be ignored in the short-run, they will be harder to ignore over a six-year period. At the very least, they suggest that the odds of above-average returns from here are low.

Borrowing From the Future if Trees Don’t Grow to the Sky

In the end, what the Fed has accomplished through the most expansionary monetary policy in history is not a new paradigm but simply a shift in the natural order of returns. In search of a “wealth effect,” they have borrowed returns from the future to satisfy the whims of today. They did so with the hope that the American people would borrow and spend more money and economic growth would accelerate because of short-term gains in the stock market.

Unfortunately, after six years, this “wealth effect” has failed to materialize, as this has been the slowest growth recovery in history in terms of real GDP and real wage growth. What we are left with is a boom only in the stock market, not in the real economy.

If trees don’t grow to the sky, then, future returns will have to suffer because past returns have been so strong. There is no other way unless you believe that multiples can continue to expand to infinity without reverting back to historical norms.

For anyone still saving and adding to their investments without having sold a single share, this has not been a gift from the Fed but a tremendous burden. The net savers have been forced to add money to stocks at propped-up levels, which will ultimately lower their long-term returns. The savers would have been far better off with a more moderate price advance with declines along the way which would have enabled them to buy in at lower prices and increase long-term returns. This is a mathematical truism.

In the bond market, math is also working against investors as the Fed has suppressed interest rates for over six years now. At the current level of 2.1%, the U.S. 10-year Treasury yield suggests that bond returns (NYSEARCA:AGG) are likely to be far below average in the years to come.

If trees don’t grow to the sky, the next six years will look nothing like the previous six and investors are likely to face a much more challenging environment. But don’t just take my word for it. I’ll leave you with a quote from Clifford Asness of AQR who had this to say in a recent interview with Barry Ritholtz:

“We find the 60/40 portfolio is about as bad as it’s ever been, prospectively” – Cliff Asness, February 21, 2015

This writing is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction, or as an offer to provide advisory or other services by Pension Partners, LLC in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Pension Partners, LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Note: here is the URL from which I took this article to share with you: http://seekingalpha.com/article/3010966-if-trees-dont-grow-to-the-sky-the-next-6-years?ifp=0