My Comments: I’ve written before about how stock and bond values are NOT joined at the hip with the state of the national economy. This essay by Lawrence Fuller suggests how that disconnect may play out for those of us with money invested in the markets.

My gut tells me the odds of there being an economic retraction in the coming months, especially taking into account what is happening across the globe, is realistic. That in turn suggests the markets will continue to contract until such time as that contraction fully manifests itself. At that point we’ll all be looking ahead to a recovery and pushing money once again into the markets, hoping for an investment gain.

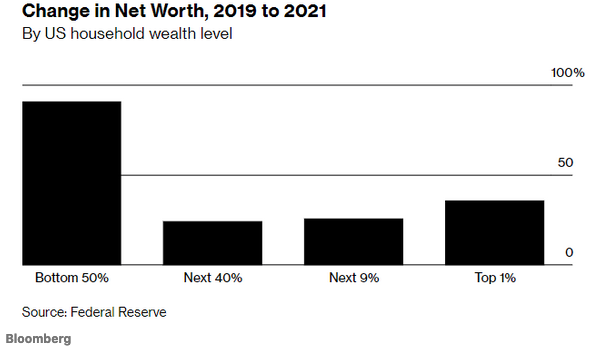

The author also points out a falsehood that says giving more money to the already wealthy leads to an uptick in the wealth of the rest of us. It doesn’t. Which in my opinion argues in favor of increasing the taxes paid by those at the top.

(Please note that I’ve not included all the images from the essay, just those I thought would be most helpful to your understanding.)

By Lawrence Fuller \ 31 AUG 22 \ https://tinyurl.com/2zj88bwe

Investors continued to be spooked yesterday by Chairman Powell’s hawkish tone. If his intention was to cool risk asset prices, the mission is accomplished. The 2-year Treasury yield hit a new high of 3.47%, which further inverted it with the 10-year, encouraging the bears to growl even louder about the likelihood of a recession. Yet the spread between the 3-month and 10-year yields is still positive, which calls into question the certainty of an economic contraction. Still, the bear market in stocks and inversion of 2- and 10-year yields has a growing consensus convinced we are on the cusp of recession. I think the consensus is misjudging the strength of this economy.

Investors typically look at the economy through the lenses of the market, which has historically served as a reliable discounting mechanism for real-world developments. Yet the Fed distorted these lenses after the financial crisis in 2008 when it decided to use the market as a tool to achieve a specific economic outcome. In other words, it manipulated interest rates and inflated financial asset values to create a wealth effect that it hoped would trickle down to the working class. In turn, that would increase the rate of economic growth, helping to achieve the Fed’s mandate of stable prices and full employment. The Fed spent years after the Great Recession trying to drive the rate of inflation up to 2% with little success. The reason its strategy did not succeed is that the primary beneficiary of its monetary policy largesse was the top 10%. This demographic owns the vast majority of stock market wealth, which it typically saves and does not spend. It never trickles down.

While the monetary stimulus in 2009 was more than adequate to produce investment returns, the fiscal stimulus was woefully inadequate to ignite growth in the economy. That is why the economic recovery that followed was one of the weakest on record with stagnant wages, below-trend growth, and a rate of inflation stubbornly below 2%. The bull market of the 2010s gave a false sense of strength in regard to the economic expansion that accompanied it.

Fast forward to the recovery that followed the pandemic-induced recession in 2020. Both the Trump and Biden administrations pumped trillions of dollars of fiscal stimulus into the economy to coincide with the monetary stimulus provided by the Fed. The result was an economic boom. The various fiscal programs certainly contributed to the high levels of inflation we see today, but they also resulted in the recession being shorter and shallower than it would have been otherwise. This is because the fiscal programs strengthened the balance sheets of lower- and middle-income households in a way that monetary stimulus cannot. It put money directly into the pockets of consumers and increased their net worth.

Bloomberg

It also contributed to wage growth, which benefited the lowest quartile of wage earners more than any other. This combination resulted in a historically low debt service percentage relative to disposable income for consumers. This is the primary reason I am far more optimistic about the economic outlook than the consensus.

Bloomberg

Following the Great Recession, the market’s stellar performance gave the appearance of a strong economy, but it was very misleading. By the same token, this year’s bear market gives the appearance of an economy on the cusp of recession, but this is equally as misleading. I think the Fed can return short-term interest rates to a level modestly above neutral and restore its balance sheet to a size consistent with the needs of a $23 trillion economy without ending the expansion. This is largely due to the size and breadth of the fiscal stimulus that was implemented following the pandemic. It is also the basis of my outlook for the June low in the major market averages being the ultimate low for the bear market behind us.