My Comments: I’m about to publish a new addition of the Dynamics of Retirement. (You’ll find the cover on the right side of this page). It has a chapter that asks How Long Will I Live?.

The Covid19 pandemic has effectively reduced the statistical life expectancy of everyone in the US. And presumably across the world also. With that in mind, and mindful that many of you, my readers, including my son and daughter, are either planning to be retired or are already retired, I began to wonder about life expectancy in general.

I found I had saved a link to a white paper published by the World Economic Forum in May of 2017. Here’s a link to what is a lengthy document: https://tinyurl.com/yc89sahx. I encourage you to click on this link and satisfy yourself that what I share with you below is accurate.

The fine print says, “No part of this publication may be reproduced or transmitted in any form or by any means…”. However, I’m willing to take responsibility if anyone files a complaint since I see this as relevant information that should be shared with anyone with any expectation of being a retired person in the years to come.

So, here’s my summary of what appears in the Introduction. You’ll have to visit the site to get the rest of it.

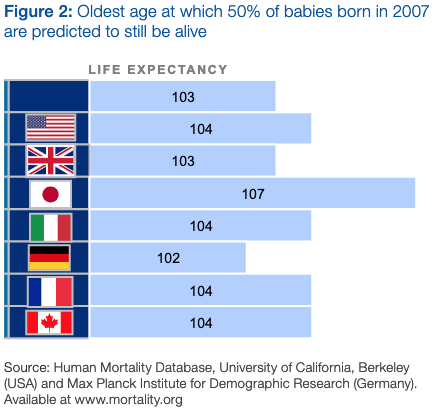

Since the middle of the last century, life expectancy has been increasing rapidly. On average, it has been increasing by one year, every five years (see Figure 1). Babies born today in 2017 can expect to live to over 100, or in other words, they will live to see the year 2117.

While increased longevity is a positive step for individual and societal health and productivity, this change has a profound impact on the traditional make-up of our societies and the social protection systems that are designed to support us in our old age.

In Japan, which has one of the world’s most rapidly ageing populations, retirement can begin at 60. This could result in a retirement of over 45 years for those who will live to the current life expectancy of 107 (see Figure 2). What is the impact of a population that will spend 20%-25% more time in retirement than they did in the workforce? How do we rethink our retirement systems that were designed to support a retirement of 10-15 years to prepare for this seismic shift?

One obvious implication of living longer is that we are going to have to spend longer working. The expectation that retirement will start early – to mid-60s is likely to be a thing of the past, or a privilege of the very wealthy.

Absent any change to retirement ages, or expected birth rates, the global dependency ratio (the ratio of those in the workforce to those in retirement) will plummet from 8:1 today to 4:1 by 2050. The global economy simply can’t bear this burden. Inevitably retirement ages will rise, but by how much and how quickly demands urgent consideration from policymakers.

Given the rise in longevity and the declining dependency ratio, policymakers must immediately consider how to foster a functioning labor market for older workers to extend working careers as much as possible. Employers also have a key role to play in helping workers reskill and adapt their work styles to support a longer working career.

This paper focuses on the sustainability and affordability of our current retirement systems. To protect against poverty in old age, we believe that retirement systems should be designed to provide a level playing field and equal opportunity for all individuals. A well-designed system needs to be affordable for today’s workers and sustainable for future generations to ensure that all financial promises are met.

Healthy pension systems contribute positively towards creating a stable and prosperous economy. Ensuring that the public has confidence in the system, and that promised benefits will be met, allows individuals to continue to consume and spend through their working and retired years. If this hard-earned confidence is lost, there is a significant risk that retirees will moderate their spending habits and

consumption patterns. Such moderation would have a negative impact on the overall economy, particularly in countries where the size of the retired population continues

to grow.

Action is needed to realign our existing systems with the challenges of an ageing population. Those who take proactive steps will be better equipped in the years ahead.

In this short paper, we will share findings on:

– The challenges we are facing and the current savings

shortfall

– System design recommendations for policymakers

– Actions for policymakers

I rather not live past my 70’s, thank you.

Still, it couldn’t hurt to plan for the possibility.

LikeLike

TN – I suspect you are not yet into your 70’s. As someone past their 70’s, I can tell you I have no desire to stop doing what I’m doing and trying to make a difference in people’s lives. My hope is that you too will feel the same way.

LikeLike