My Comments: No, Vanguard is not saying there’s about to be a market crash. What they’re saying is that over the next decade or so, the return on investment we’ve been used to over the past decade is likely to be a lot lower.

This is something those of us in the investment advisory business have heard for a long time. And frankly, it’s led to a lot of doubt over the past few years when the market refused to settle back to historically “normal” returns. Instead, it’s just kept going up and up to the point where it’s almost irrational.

Depending on your current age, and to the extent you have money growing and accumulating to help you pay your bills when you quit working, what Vanguard says is cautionary. And depending on how long you live AFTER you quit working is how concerned you should be.

by Alpha Gen Capital \ 29 OCT 2021 \ https://tinyurl.com/8trha7s

You cannot know the future

No matter how much you research or how high your conviction may be, forecasting will always be more art than science.

Recently, Vanguard wrote a blog post titled “Tuning In To Reasonable Expectations” which elaborates on what investors should be expecting.

Additionally, Natixis put out a study on investor expectations over the summer that had some stunning results. It showed US investors expect to achieve 17.5% returns over the next 5 years.

It just so happens that the trailing 5-year annualized total return is 17.3%. In other words, investors are simply extrapolating past returns into the future, in perpetuity.

They will be sorely disappointed.

So, investors expect higher returns at the same time that the long-term data indicate that returns will be below normal. Hold on. It gets worse.

The average equity allocation today is at the highest level in two decades. This is one of the greatest indicators of stock market and the foundational work of an anonymous blogger under the pseudonym, Philosophical Economics Blog.

Mark Hulbert of Hulbert Ratings calls it the greatest stock market indicator that he has come across when predicting the S&P 500’s total real return over the subsequent ten years.

He wrote:

The average household’s portfolio allocation to equity currently stands at 50.9%. As you can see from the accompanying chart, below, it is a contrarian indicator, with higher allocations associated with lower stock market returns over the subsequent decade. The current reading is higher than all but one period since 1951.

That lone exception came in the first quarter of 2000, right at the top of the internet bubble. That quarter’s reading stood at 51.8% – just 0.9 of a percentage point higher than the latest reading.

How bearish is the indicator currently? According to a simple econometric model based on the historical relationship between the indicator and the stock market, the indicator is projecting that the S&P 500 will produce a total real return of minus 4.2% annualized over the next decade.

Let’s get back to Vanguard.

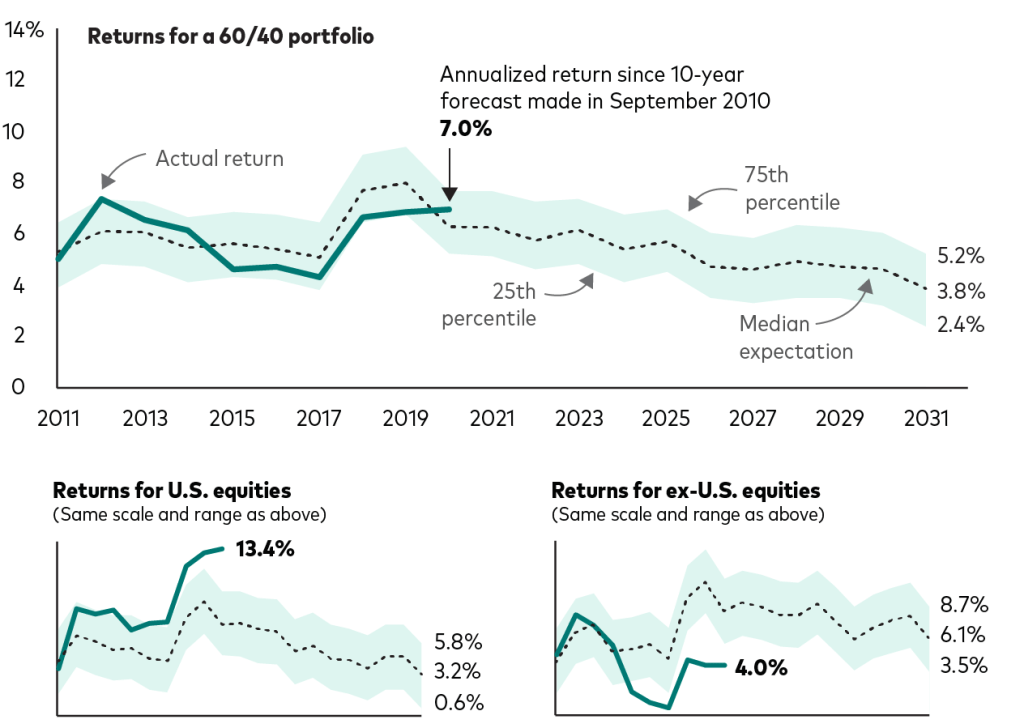

They see much lower returns ten years from now on a trailing basis. Just 3.8% annualized total returns are what they expect from a 60/40 portfolio. That is about half of the trailing 10-yr number today.

(Source = Vanguard)

Worse yet are the returns expected for the US piece of the asset allocation which is expected to be just 3.2% compared to 6.1% for the ex-US portion of the portfolio.

You can see from the bottom two charts above that US stocks have deviated above their forecasted mean and that International stocks have deviated below them. To me, that indicates you should be starting to skew your portfolio more towards international stocks.

It Gets Worse…

Investors need to really dig down deep and figure out if they can handle more risk or not. The same portfolio two decades ago today would generate about half the return with about 20% more risk. The 4% rule has been thrown out the window since 4% is becoming harder and harder to come by.

The 4% rule was fairly easily to satisfy in 95%+ of outcomes simply from the fact that the income piece of the portfolio was generating yields in excess of 6%. For those withdrawing 4% of their portfolios each year they could invest 100% of their assets in 6% yielding, lower-risk securities and reinvest the excess to account for inflation.

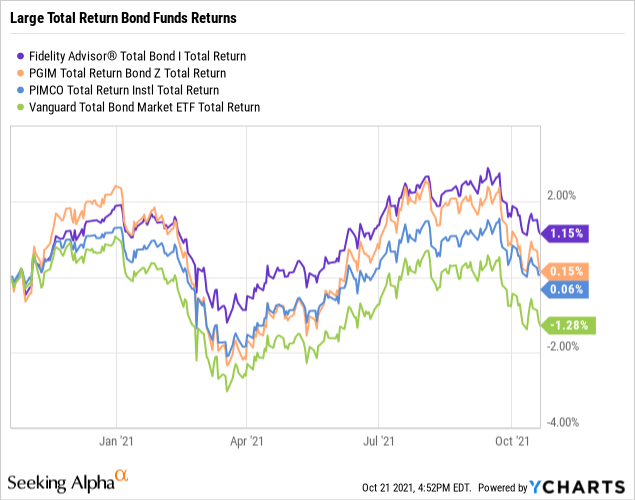

Today, the bond sleeve of the portfolio of one’s portfolio meant for income will produce very little of that. Total return bond funds will produce 1-2% returns, if you’re lucky, over the next 3-5 years. If you don’t believe me, check out what they’ve done for the last year already: -1% to 1.1%.

(Data by YCharts)

The question investors in these funds for the ’40’ in their 60/40 will need to ask themselves is, “why bother?” Is this just a defensive piece of the portfolio? If so, why not just keep it in cash and remove the interest rate and credit risk. You’re not earning much more than that anyway!

Structuring A Portfolio For The Future

We have entered a new paradigm. That cannot be said enough. This new paradigm will require new thinking.

The problem is that so many investors are stuck in the old paradigm and old portfolio construction techniques. Those techniques worked so their thought is, why change anything?

Future returns that we went through earlier are screaming to us that valuations, interest rates, and other variables are highly to depress those gains.

Building a portfolio based on long-term historical averages is like dressing every day based on the average climate of the region.

For investors who only look back, they may be surprised what their accounts over the next ten years compared to the last ten.

New portfolio theory suggests blending traditional assets with tactical, alternative, and esoteric strategies. While these still add risk to the overall portfolio, the added return more than compensates them for the added volatility.

Some alternative assets include real estate, private markets, long/short, market neutral, commodities, and arts & collectibles.

For real estate, I’m not really talking about publicly traded REITs – though they can be used as substitutes. These are really esoteric investments and there are more and more coming to the retail investor each day. We will continue to highlight them.

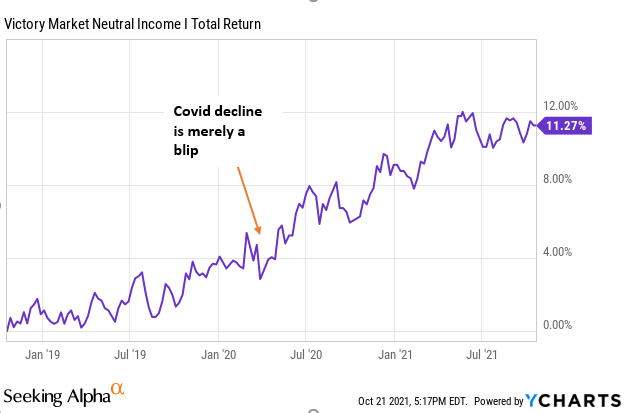

One example would be the Victory Market Neutral Income Fund (CBHIX) which is a lower risk cash/bond substitute. It yields 2.7% and has a longer-term track record of producing >4% total returns over the last 3- 5 years. The amount of risk is very low here.

Adding these pieces to your bond sleeve can help produce much better returns without taking on substantially more risk by shifting more to stocks. As the Vanguard study shows, US stocks (which I tend to see as massive overweights in individual portfolios today) are going to be the worst place to be.

But bond predictions are fairly easy. Your total returns are going to be much lower than you think. When that money starts to come out to find a better home as investors get frustrated and make mistakes, where will it go?

I do think some will move into areas we discuss below. If you can be first, then you can catch a tailwind from the flow.

The New Portfolio

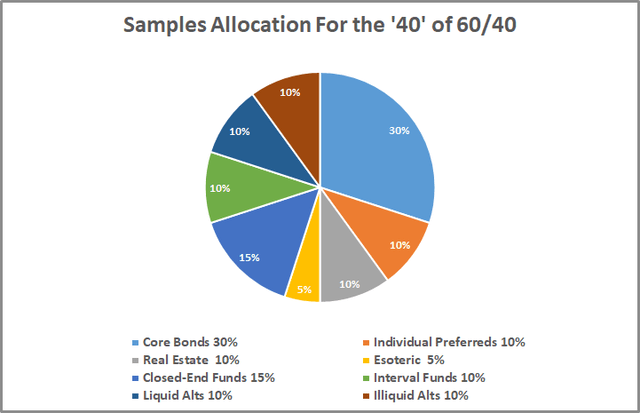

I’ve posted this before and there is definitely no hard and fast rule on what the breakdowns should be. However, you have to consider the risks given they can differ significantly. Obviously, 100% in core bonds vs. 100% illiquid alts or junky individual preferreds will have very different risk profiles.

These portfolio segments can be public or private:

- Core Bonds: Traditional assets in the bond space. Think, for example, “ABC Total Return.”

- Real Estate: Talking about non-publicly traded positions. YieldStreet is a good example.

- Esoteric: Think of investing in wine or artwork.

- Interval Funds: An improvement on the traditional mutual fund but you give up some liquidity

- Closed-End Funds: Far superior fund structure. Publicly traded. Fairly liquid. Easiest way to access private markets.

- Liquid Alts: ’40 Act fund hedge fund strategies in a mutual fund structure.

- Illiquid Alts: Private debt and private equity typically through an LP structure (K-1s)

- Individual preferreds: Single preferred stock issues held for the 4.5% to 6.5% yields. Quarterly payers. Less liquid. We like high-quality preferreds of CEFs.

For years, the 60/40 was a go-to for investment assets: 60% equities, 40% fixed income. A diversified basket of stocks gives you growth potential, and the bonds give you safety and ballast.

Though it is NOT dead, it is going to produce far different results than it did for the last four decades. Investors who need more than what Vanguard is expecting for the next decade of 3.8% per year will need to shift to a new paradigm of thinking for their portfolios.

The Yield Hunting Core Income Portfolio System

- Are you afraid of equities at these lofty valuations?

- Do you want to create a monthly paycheck for yourself with less risk?

- Have you been interested in Closed End Funds but never investigated further?

Well, Yield Hunting can help you construct a core bond portfolio, either to expand your fixed income side of your portfolio, or simply reduce risk. Check out our marketplace service that helps investors structure their non-equity portfolios and gear it for maximum income production without taking excessive risks.