My Comments: Once you reach adulthood, there are, in my opinion, three fundamental phases of life to experience. I refer to them as the GO-GO years, the SLO-GO years, and the NO-GO years. If you’re still in your GO-GO years, you should be to thinking about the next two phases.

To a large extent, the following thoughts from Cory Clark will help define how you live your life once the GO-GO years end.

By Cory Clark \ 8 SEP 2021 \ https://tinyurl.com/ygt5cmff

“If you fail to plan, you’re planning to fail.” These words, from the immortal Founding Father Benjamin Franklin, have been recited countless times over centuries to inspire a thoughtful approach to our most important endeavors. Apparently, Ben Franklin, who knew a thing or two, felt that flying by the seat of your pants was unlikely to yield a successful outcome.

Few would quibble with this notion, but in our day-to-day lives, we sometimes fall victim to the extemporal pursuit of a goal. Perhaps we’re just so excited to move forward that we hastily bypass planning and jump in headfirst. Or maybe the task seems so daunting, that planning is scary and it’s easier to simply close our eyes and put one foot in front of the other. Unfortunately, some Americans are saving for retirement with their eyes closed and Ben Franklin would not approve.

Imagine having a goal and not knowing where you stand, where you’re going or if you’re even on track to meet the goal; sounds crazy right? As whacky as it sounds, it’s not that uncommon for Americans saving for retirement, particularly those doing it themselves without professional help. But if you don’t know the answers to these basic questions, are you doing it yourself, or just not doing it at all?”

DALBAR, Inc., a leading researcher in investor behavior recently studied 1,103 investors to gain insight into their retirement planning (or lack thereof). The study found that more than half (53%) had not developed a financial plan to fund their retirement in the last 5 years. Not surprisingly, most of those investors were do-it-yourselfers. The study found that 75% of investors with a financial advisor had developed a plan to fund their retirement in the last 5 years while less than a third (30%) of those without an advisor have developed a plan. Simply put, it’s uncommon for people to develop and maintain a retirement plan on their own.

This highlights a less talked about value of the financial professional. Advisors are looked to as a guide to the right investments and/or allocation, but an advisor’s value starts at a more basic level: helping one to answer “The 3 Fundamental Questions of Retirement Planning”: (1) where am I? (2) where do I want to go? and (3) am I on track to get there?

Fundamental Question #1: Where am I?

When considering the 3 fundamental questions, our current position is a natural place to start. To plan for a goal, we must first identify and understand our starting point. Our current position in our journey should be the easiest of the 3 Fundamental Questions to answer, and it is. In 2021 we are just a few clicks away from seeing any of our investment account balances. However, for some investors, identifying a starting point has been a non-starter in their retirement planning.

DALBAR’s Retirement Planning study found that 14% of investors don’t know what they currently have saved for retirement. Those working with a professional are less likely to have such a blind spot (only 7% do not know what they currently have saved) than those who do not work with an advisor (17% do not know). While these proportions are not large, the essential nature of the question alongside the ease in which it can be accessed seem to be a foreshadowing of problems investors may run into when addressing more complicated questions like how much will I need to retire? and Am I on track to get there?

Fundamental Question #2: Where do I Want to Go?

You don’t have to be smart enough to invent electricity (that’s the last Ben Franklin reference, I promise) to know that you can’t plan for a goal if you don’t know what the goal is. Many self-help gurus will emphasize the importance of seeing and visualizing the goal at hand. It stands to reason that on the path to a dignified retirement, one must understand what a dignified retirement means to them and what proportion of their current income they want to replace at retirement to achieve it. This is a simple thought exercise that requires some brainstorming, but no special expertise or sophisticated software. It does require one to go through the process and 39% of Americans have not gone through that process. Of the 3 Fundamental Questions, this is the one for which the most Americans had no answer.

On the surface, it would seem that nobody needs an advisor to estimate the level of retirement savings needed. After all, nobody else could understand an investor’s spending habits or vision for their future better than the investor. However, there are many uncertainties that complicate the process of coming up with an accurate estimate, such as future inflation, healthcare needs, insurance coverage, living situation, etc. All these uncertainties may be acting as a barrier for some to come up with any estimate at all.

Working with an advisor should help to make the estimate more accurate, but the presence of an advisor increases the likelihood of having an estimate at all. More than 7 out of 10 individuals with a financial advisor have an estimate of what they’ll need for retirement while only 4.5 out of 10 DIY investors have identified a retirement savings goal. In summary, it’s uncommon for people to estimate their retirement savings goal on their own.

Fundamental Question #3: Am I on Track to Get There?

Answering this question is a little more intricate, as it requires a projection of where one will be at some future date. Such a projection may require a digital tool or some degree of financial expertise. If a projection of retirement savings at the desired retirement age has been made and it’s greater than or equal to the answer to Fundamental Question #2, the investor is on track; if not, changes should be considered.

Twenty-two percent (22%) of investors do not have an estimate of what they will have saved at retirement. For these investors, they have not projected where they will be at retirement and therefore have little basis to determine whether they are on track or what changes to make. One can only hope that the answer to this question is favorable. If it is not, it will remain unchecked until the 3 Fundamental Questions of Retirement Planning are answered.

The third fundamental question is no different than the previous two in that the use of a financial professional makes an investor more likely to have an answer. Those without an advisor are 3 times more likely to not have an estimate of what they’ll have saved at retirement. Less than 10% of investors with a financial professional do not have an estimate of what they will have saved at retirement while 30% of do-it-yourself investors lack such an estimate.

Ignorance is not Bliss

Is it true that those who fail to plan for retirement are planning to fail? Or perhaps the more direct question is: will they fail? DALBAR’s Retirement Planning Study did not calculate a likelihood of retirement success for each respondent. However, respondents were asked about their overall satisfaction with their retirement savings and the study found that not knowing the answer to one of the 3 Fundamental Questions of Retirement Planning led to lower satisfaction with one’s future financial outlook.

Investors generally have some degree of satisfaction with their retirement savings, but few are very satisfied. In fact, investors are most likely to be “Somewhat Satisfied” but least likely to be “Very Satisfied.” More than a quarter of investors are “Very Dissatisfied” with their retirement savings, the second most common disposition.

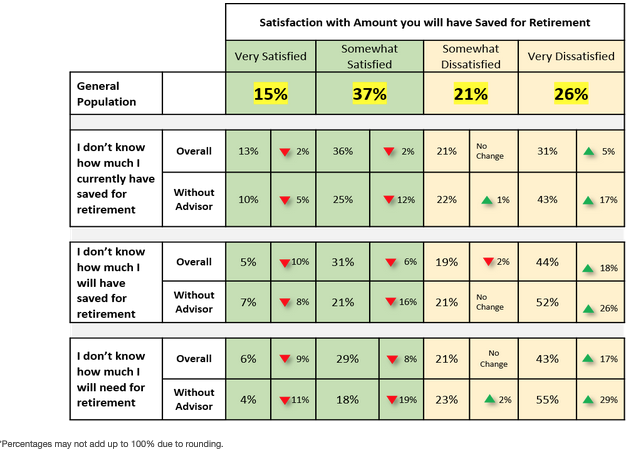

The table below displays the satisfaction with retirement savings for all investors in the study (General Population) versus those who had unanswered Fundamental Questions of Retirement Planning, further segmented by those without the help of a professional.

What we see from the table above is that those with unanswered Fundamental Questions of Retirement Planning tend to be less satisfied in their retirement savings. This is not to imply causation because it’s a classic “chicken and egg” scenario where it’s unclear whether unanswered questions lead to dissatisfaction or if dissatisfaction leads to not pursuing answers. Regardless of which is the chicken, and which is the egg, those who are dissatisfied will have a hard time making meaningful changes without the answers to the 3 Fundamental Questions of Retirement Planning.