My Comments: The words below come from a group called Tactical Fund Advisors. I’m not promoting their use but given where the markets have come in the past decade, I think it’s prudent to think life will return to normal, a normal that includes market pull backs.

It may not be a roaring crash, but it is very likely to be a significant event that may last for several months or more. I have no idea when it will happen, just that it will. These folks think it’s likely to happen before we’re ready for it.

If you’re someone like me who is retired and living off past work/life efforts, and to the extent you have financial reserves needed to pay your bills in the future, it’s very important you remain cautious.

By Michael Morton \ 24 MAY 2021 \ https://tinyurl.com/4ppxuwze

Just Friday, the Bureau of Economic Analysis reported that first-quarter Growth Domestic Product (GDP) grew at an annual rate +6.4%. In addition, manufacturing and service indices are the strongest they have been in nearly forty years, corporate earnings continue to surprise to the upside, and a multi-year national infrastructure plan is in the works.

However, as we sit one-full year from the pandemic lows, and after a historic rebound, we continue to be on the lookout out for any potential change in market character or investor sentiment. After all, as a tactical investing proponent, it is our goal to preserve client capital as much as it is to grow it. In that vein, here are nine reasons why a market pullback may be due… And one reason not to worry!

#1. Stock Valuations Are Lofty

The total return adjusted stock Price/Earnings ratio for the S&P 500 is now above 38 on the global economic re-opening. Although not quite at pre-tech 2000 bubble levels, this leaves valuations in their 98th historical percentile, placing continued growth and contained inflation under the microscope each quarter ahead.

Looking at the broad market, the story is similar. Below is a chart of the P/E ratio of the Value Line Index back to 1980, which, as you can see, is at extremely high levels.

In addition, other metrics, such as the Price-to-Sales ratio (chart below) also suggests valuations, as well as a variety of technical indicators, including distance from the 200-day moving average, are at extreme levels.

To be sure, valuations can remain elevated for quite some time, as seen in 2004-2007 in the first chart above. However, we feel it is important to recognize that the overvalued condition seen in the market, which is evident across nearly all traditional metrics, suggests that market risk is elevated at the present time. And although overvaluation is most definitely not a signal that a correction is imminent, it does tell us to be cognizant of the risk/reward environment.

#2. The Frenzied Nature of the Market

Besides lofty valuations, we have SPACs (Special Purpose Acquisition Company) going crazy with 311 new SPACs issued in 2021 alone. These “blank check” companies are hurting Private Equity firms as far as investing for deal flow. Warren Buffett calls them “Killers” (Yahoo Finance, 5/3/2021). There are also high valuations and tremendous amounts of IPO’s over the past year. There has been several government stimulus packages made available to individuals and corporations (and an expected $2T more). Residential real estate is soaring in value over the past year and now. Commodities are also very expensive today which is cause for inflation concerns.

So several asset classes are correlating to the upside. Therefore, being a tactical investor makes sense with TFA.

#3. Earnings Comparable Will Get Tougher

As we have stated, markets have made a historic recovery since the lockdowns have lifted. However, at some point in the months ahead, the year-over-year earnings comparisons, which are currently well above expectations, will become much more difficult to match. The market is ultimately a forward discounting mechanism, and with stocks arguably “priced to perfection,” any disappointment on the earnings front would be certain to catch investors’ eyes.

#4. VIX Levels Suggest an Unprepared Market

CBOE Volatility Index (“VIX”) levels are well below twenty now. While this feeds into our long-term forecast for market stability, it likewise signals that market participants may not be prepared for any unexpected news flow. We all know that, ultimately, markets can “correct” with or without a “trigger.” However, on top of any possible unforeseen black swan event, we continue to face the very real possibilities of a rise in Covid rates here or abroad (see the dramatic surge in cases in India), and/or a resumption of the march higher in long-term interest rates. Yes, these are known risks, but it seems to us markets have been lulled into a sense of complacency by the incredible post-election momentum, and we simply are not out of the woods just yet!

#5. The Market Has Had At Least One 6.5% Pullback Each Year Since 2000

That is right, a 5% to 10% retrace in the S&P 500 index at least once per year is very normal, and in fact, we have seen one such “pullback” each year over the past twenty. The surprise here would be if we do not see the bears come out of hibernation – even for a short period – sometime in 2021.

#6. Seasonal Tailwinds Will Become Headwinds

Many of you are likely familiar with the “Sell in May” effect. Yes, it is real; historically, May 1st through October 31st represents the weaker half of the year for stock market performances. In addition, 2021 is the first year of a presidential cycle, which is often negative. While there has been a lot of hype over the infrastructure proposal, for instance, did you happen to take note of the embedded corporate and wealthy filer tax hikes? For the moment it is all hypothetical, but if those get closer to reality, it could certainly affect the tone of the market.

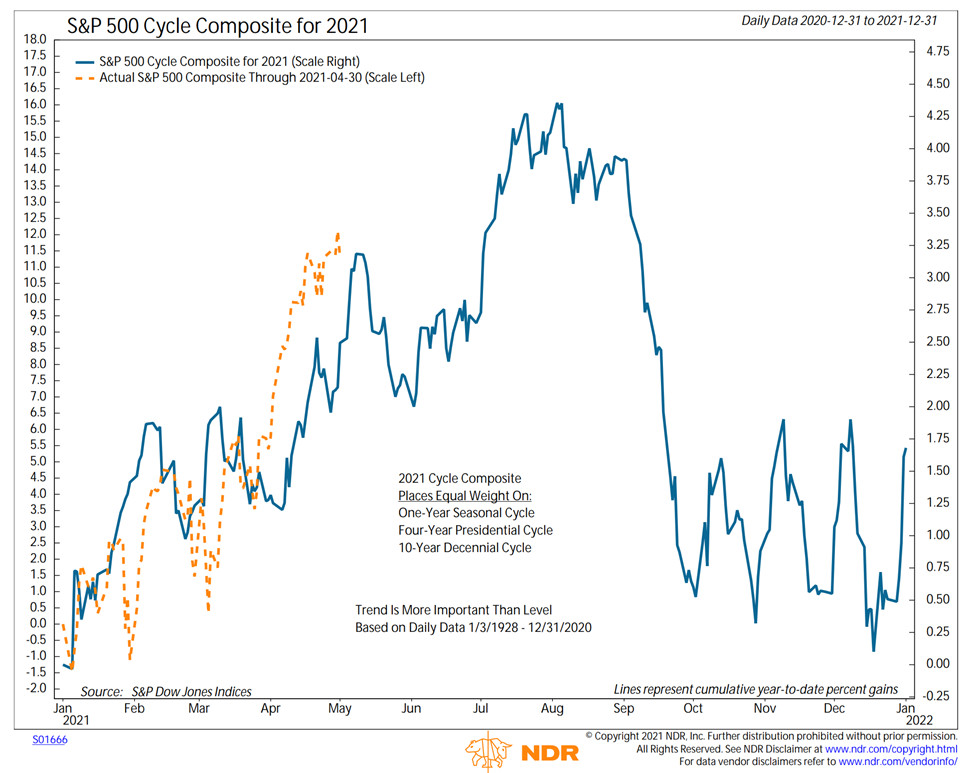

For example, below is a “mashup” of the historical One-Year, 4-Year Presidential, and Decennial cycles put together by Ned Davis Research Group. The blue line is the cycle composite’s projected market pattern for 2021 and the dashed orange line is the actual movement of the S&P 500.

While the market does not always follow history or repeat cycles exactly, we have found over the years that the historical patterns oftentimes “rhyme.” Thus, the cycle “mashup” can be eerily good at projected what to expect over the course of any given year. And this year, the cycle projections call for a rather stiff pullback once the traditional “summer rally” runs its course.

Next is our largest concern for the moment – simply that we would be hard-pressed to find a professional that is not onboard with an optimistic outlook for US stocks. And when all market participants get on the same side of a consensus trade with stocks and bonds both as expensive as they are, it often ends poorly.

#7. Everyone Is on the Same Side of the Trade

Next is our largest concern for the moment – simply that we would be hard-pressed to find a professional that is not onboard with an optimistic outlook for US stocks. And when all market participants get on the same side of a consensus trade with stocks and bonds both as expensive as they are, it often ends poorly.

#8. Inflation May Not be Transitory

Don’t look now fans, but the prices of lots of “things” are moving up – in earnest. Exhibit A is the price of Lumber, which is now several times what it was at the end of last year. Next, we note that Copper recently hit its highest level in nearly 10 years. Home prices are gaining at the fastest rate in 15 years. On Friday, we learned that the Federal Reserve’s preferred measure of inflation (PCE – or Personal Consumption Expenditures) saw the biggest monthly gain since 2009. And the Employment Cost report displayed the best quarterly wage growth since 2001.

We feel the key here is that the Fed, and in turn, the current market narrative, expects the long-awaited rise in inflation to be temporary. But, many economists disagree, contending that the rise in costs will become more “sticky” going forward. As such, the Fed – and again, the markets – may be forced to deal with a different type of inflation “problem” in the future. As in too much inflation. Something that hasn’t seen in a very long time.

#9. All Good Things Come to an End, Eventually

It is safe to say that the economic data and corporate earnings have been surprisingly strong so far in 2021. However, it is important to remember that both the federal government and the Federal Reserve have played a large role in “goosing” growth to move the economy up and out of the COVID-induced hole as fast as possible. The key point is that the current rate of growth for both the economy and earnings is likely unsustainable. Thus, at some point, the forward-looking stock market will have to deal with slowdowns on several fronts.

First, both economic and earnings growth should begin to slow as the global economy returns to some form of “normal.” In addition, Jerome Powell’s Fed will have to return monetary policy to a more normal state, which, in this case, means “tapering” the current bond-buying program and raising rates. And it should be noted that all the above has tended to create less-than favorable environs for the U.S. stock market.

But… Did We Mention the Economy Is Good?

We started this article talking up the economy, and this is where we will leave. Despite the myriad of reasons laid out as to why we should expect to see a garden-variety pullback in the weeks/months ahead, the second year of a bear market recovery generally continues to bring positive, if not more muted returns featuring modestly higher volatility. And so far, at least, that is exactly where we are at.

All that said, as we also stated, we are market tacticians first and foremost. By being agile in selecting sectors, styles, and levels of exposure, our strategies are designed to dynamically adapt to whatever markets “cards” are dealt. And this, dear reader, is one key reason to not fret too much over the idea of a correction.

It shouldn’t matter, whether you are retired or not…..the market pulls back 15% on average every year, and 30% every five years. Of course we are going to have a crash or pullback. If you are 60, you’ve got 6 more “armageddons” in your lifetime……..cash reserves, proper allocation, done. Wall Street is full of it.

LikeLike