My Comments: The following about annuities was written by Joseph M. Maas, a financial professional located in Seattle, WA. He has multiple credentials attesting to his financial expertise and is associated with an SEC Registered Investment Advisory firm. His title to the white paper he’s written differs slightly from mine.

As someone who has attempted to write about the viability of annuities when building a portfolio to last one’s lifetime need for retirement income, I encourage you to read to the end if you have plans to retire soon or are already retired. This is very good information.

by Joseph M. Maas \ 21.01.27 \ https://tinyurl.com/y4ohtfhz

Fixed annuities may be one of the most misunderstood investments in the investment advisor’s portfolio, but they have their place in the asset allocation decision. The goal of this paper is to explain a new approach to incorporating fixed annuities and fixed index annuities in a portfolio as an asset class.

The portfolio manager’s goal may be to determine a portfolio composition that produces the best risk-return profile to achieve the client’s financial objectives. In the following approach, the portfolio allocation to annuities is based on their relationship in the risk return goals of the portfolio. It is a fiduciary process that takes advantage of the benefits annuities offer, balanced with the risk tolerance and return requirements of the investor.

As an asset class, fixed annuities tend to be low risk, low return, but they are also a means of offsetting longevity risk – the risk that you will last longer than your money. Annuities are the only financial investment that can guarantee an income flow for the duration of the individual’s life. With that said, an annuity is not appropriate for every investor. In most situations, annuities are best implemented as an additional asset class to a diversified portfolio allocation, not as the mainstay of a portfolio.

UNDERSTANDING THE FIXED ANNUITY

A fixed annuity is a contract between the annuity holder and an insurance company to cover specific goals. Both parties are locked into contractual obligations. In exchange for a lump sum contribution or a series of contributions to the contract, the annuity company will pay a guaranteed rate of interest…usually a higher rate of interest than CDs or other traditional investments due to an annuity’s long-term nature, for a set period of time. In the accumulation stage, the annuity is earning and reinvesting interest. In the payout stage, the contract holder chooses how the return of principal and interest will be made.

Depending upon the annuity contract, annuities can be structured to provide payments for a fixed number of years to the contract holder and his/her heirs; for the individual’s lifetime; until the individual and his or her spouse has passed away; or a combination of both lifetime income and a guaranteed “period certain” payout. A “life with period certain annuity” pays income for life, but if the individual dies during a specified time frame, beneficiaries receive the remainder of the payments for the contractual period chosen at the time of application.

Fixed annuities come in two basic styles:

(1) Fixed interest rate annuities, and

(2) Fixed index rate annuities.

A fixed interest rate annuity, commonly referred to as a fixed annuity, is the simplest type of annuity contract, offering safe, but low returns and tax deferral. It usually matures after anywhere from one year to ten years. The contract holder knows the annual interest rate and the exact worth of the investment at the end of the term. In most cases, the annuity will automatically renew at a revised interest rate unless funds are withdrawn or moved. As long as there are no withdrawals, the result is entirely predictable.

A fixed index rate annuity allows for the potential of higher interest returns without exposure to the market risk by linking…not investing…to a stock market index such as the S&P 500, NASDAQ 100 or other equity, fixed income, or bond index offered by the annuity provider. The index annuity guarantees a minimum annual return (typically lower than a fixed annuity), safety of principal if held until the surrender period is up, and a participation rate: the percentage of the index’s return the insurance company credits to the annuity. A number of factors influence how much that return is, including:

How the index is tracked:

The cap rate: upper limit on return over a certain time period

Participation rate: percent of the index’s return credited to the annuity

Spread/margin/asset fee

Bonus: percentage of first year premiums received added to the contract value (typically subject to a vesting period)

Riders, covering extra features

It is possible, depending upon the structure of the index annuity, that over an extended period that includes market losses, an investor may experience little if any gain in the value of the annuity and could actually lose money if assets are withdrawn before the surrender period is up.

The complexity of index annuities makes it essential that investors work with advisors who take a fiduciary approach to the annuity allocation and can evaluate and compare potential returns of competing index annuity structures. A fiduciary has both a duty of loyalty and a duty of care. The advisor is required to put the interests of the client above his or her own. Any conflicts of interest must be eliminated. To the extent conflicts cannot be eliminated, they must be minimized and fully disclosed. The duty of care also requires the advisor to give advice only if he or she is qualified to do so.

CAUTIONS WITH RESPECT TO ANNUITIES

An annuity is only as good as the insurance company’s ability to honor its commitment. Before entering into an annuity contract, it is essential to determine the financial strength of the insurance company.

Because returns from an annuity are tax deferred until they are withdrawn, the IRS imposes a 10% early distribution penalty on interest earnings withdrawn before age 59 ½, similar to tax-deferred retirement accounts.

Annuities have limited liquidity and are intended as long-term investments. While many annuities allow the withdrawal of some interest earnings (generally up to 5 – 10% per year) without a penalty, (taxes and early withdrawal penalties may apply), there is usually a surrender charge for early withdrawals above that amount. Typically, this surrender charge is a percentage of the amount withdrawn, gradually decreasing over a 7 – 10 year period until it is gone.

As an insurance product, fixed annuities are not regulated by the U.S. Securities and Exchange Commission (SEC). Promotional information may not be comprehensive of the risks and return offered by an annuity. It is important to not only work with a financial advisor who is a fiduciary, but also one who is experienced in analyzing annuity structures.

To facilitate their use by investment advisors, annuity providers have developed fiduciary annuities with no surrender charges, as well as products with lower fee structures. Your financial advisor can direct you toward the appropriate annuity structure for your situation.

BENEFITS OF FIXED ANNUITIES

Low risk, guaranteed return.

Predictability. Unlike investments subject to market cycles, the investor knows how much the annuity will be worth at maturity.

No IRS contribution limits. The only limiting factor is the amount of premium an insurance company is willing to accept for the same individual.

No minimum required distributions, unless an annuity is held in a retirement account.

Tax advantaged saving through tax deferral of earnings until withdrawn, enhancing compounding growth.

Higher rates of interest than CDs or other traditional guaranteed instruments.

No probate if the annuity holder dies. Money goes straight to the beneficiaries on the contract.

Convertibility to a retirement income stream.

INCORPORATING ANNUITIES IN THE PORTFOLIO ASSET ALLOCATION

Developing an optimized portfolio is a strategic process that begins with two factors:

The client’s Investment Policy Statement (IPS)

Capital market expectations

The Investment Policy Statement is a written document that guides the management of the investment portfolio. It typically defines general investment goals and objectives; sets risk tolerance limits; describes strategies to be used in managing the portfolio; establishes types of assets that will be used; provides investment parameters and limitations, and sets liquidity requirements. An IPS is not a financial plan, although it may be part of the broader financial

plan. By setting expectations, it provides the investor a disciplined structure for evaluating portfolio performance and guidelines for the manager for acceptable investments.

Capital market expectations define the potential risks and returns of entire classes of investments, as opposed to specific investments. These expectations are used to establish an optimal blend of investments that will balance the expected risks and returns to achieve investment goals. The process starts with analysis of the real return and risk of asset classes over the past 5, 10, 25 years. Returns are then evaluated in context of the current economic environment, business and market cycles, technological changes, geopolitical factors and more. This structural approach defines the economic drivers of return and risk for individual asset classes and gives the portfolio manager a basis upon which to create an asset allocation.

With respect to fixed index annuities, capital market expectations also guide the selection of market indexes to use in the annuity, ranging from equity to bond market indexes.

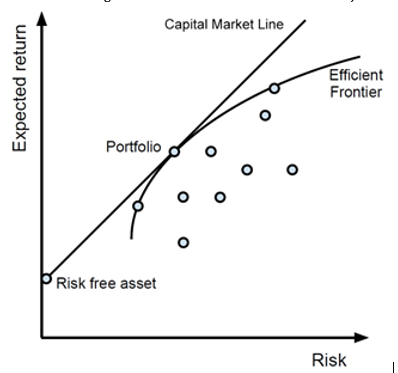

Asset allocation modeling programs are used to develop the recommended portfolio mix with fixed annuities utilized as an asset class option based on their risk return characteristics. The process determines if an annuity is right for the portfolio and how much should be included. Allocating lighter or heavier annuity exposure is evaluated with respect to the potential impact on the portfolio. Rather than a sales decision, the use of an annuity becomes an optimization decision that looks at its value to the portfolio as a whole. Does the annuity help portfolio diversification and risk management? Math and science make that decision.

Monte Carlo simulation allows the manager to further evaluate a range of possible outcomes and the return probabilities of different allocation mixes from extreme possibilities to possible consequences for middle-of-the-road decisions. The ideal portfolio is the point on the efficient frontier that is tangential to the investor’s return and risk objectives.

MAINTAINING THE ANNUITY ALLOCATION OVER TIME

Because capital market expectations will change in response to new market conditions, appropriate asset allocations will also change over time. Market cycles, geopolitical shock, monetary policy shift, regime changes, and other factors influence market risk and expected returns. Asset class performance within the portfolio will also shift allocation balances. Rebalancing may be required if the math says the portfolio no longer aligns with the efficient frontier.

While a new client and a new portfolio may merit a different allocation, changes in existing portfolios should always be based on asset valuation, correlation and variance relationships among asset classes and trading costs including taxes and fees. If rebalancing is not expected to provide greater return, change may not be the right decision.

Reallocating within the framework of annuity is a slower, more strategic decision, requiring evaluation of the costs of changing the allocation with anticipated benefits. Risk on or risk off optimization is a consideration. Does it make sense to increase the annuity position? Should the manager consider changes within the annuity’s structure, such as modifying the index used in a fixed index annuity? What impact will surrender charges have? Have changes in the interest rate environment created opportunities for greater returns that outweigh the surrender charge to withdraw funds from the annuity? Are penalty free withdraw strategies available? Can penalty free systematic withdraw strategies be used?

REALITIES OF PORTFOLIO DIVERSIFICATION

When annuities are redefined as an asset class, their use is based on whether or not they are appropriate for the portfolio and whether they provide reasonable insurance against longevity risk and reduce overall portfolio risk.

“Knowing our risks provides opportunities to manage

and improve our chances of success.”

Roger VanScoy

Diversification’s value as a risk management tool is its potential to reduce portfolio losses in a severe market downturn and give the portfolio a better chance to recover quickly from losses. To do so, the portfolio is invested in asset classes that are expected to move inversely at different stages of the market. Fixed annuities are a true diversifier because they are not highly correlated to other asset classes. Market cycles have minimal impact on the value of the annuity because they are bound by zero loss.

Risk at its most basic level is the loss of one’s investment. Because a fixed annuity guarantees preservation of principal and a contractual rate of return, its value can never go to zero barring the failure of the underlying annuity company.

As much as investors might want high return with low risk, it’s comparable to a pink unicorn. It doesn’t exist. Adding a low-risk annuity can actually lower the portfolio’s required return because less return needs to be built-in to withstand market shocks. The fixed annuity as an asset class usually provides a better than money market or cash rate of return with the option of lifetime income. When the contract is annuitized, payments are set based on life expectancy of the contract holder. Outlive that expected lifespan and the long-term return on the contract looks much better. When structured properly, longevity risk is assumed by the annuity company.

While annuities are not suitable for every portfolio, their benefits merit a hard look when creating asset allocations. In the end it is a question of math. Does the annuity add value to the portfolio? Is limiting longevity risk of benefit to the investor?