My Comments: Please understand the following article comes from an established financial professional with a far better understanding of markets than mine. He also offers 5 specific positions that he thinks will outperform going forward that I’ve NOT included here.

If you want to know what they are, I leave it to you to visit the URL where I found his article. It’s the active link that follows just below. I share this with you to help you gain insights into what MIGHT happen in the near future.

By Mott Capital Mgt. \ May 16, 2021 \ https://tinyurl.com/hvy33sn4

The week of May 17 will feature two big events, the FOMC minutes and the monthly options expiration. Both are likely to have a directional pull on the S&P 500 and the broader equity market. The Fed minutes will come on Wednesday afternoon and may give investors a glimpse into what the Fed is thinking about regarding tapering or a change in current monetary policy.

Slowing Growth and Higher Prices

The market clearly thinks that bad news is good news. As the more bad economic data that comes in the more likely it is the Fed will not taper. That seems to be what happened on May 14 as stocks applauded the weaker-than-expected retail sales data while ignoring the higher inflation rates. This week’s weaker data strengthens the message from the past few weeks of slowing growth. Earnings estimates continue to indicate that growth is being pulled forward into 2021 from future years.

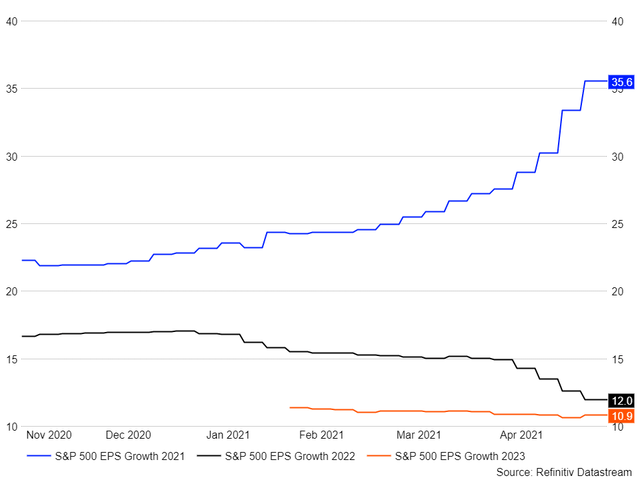

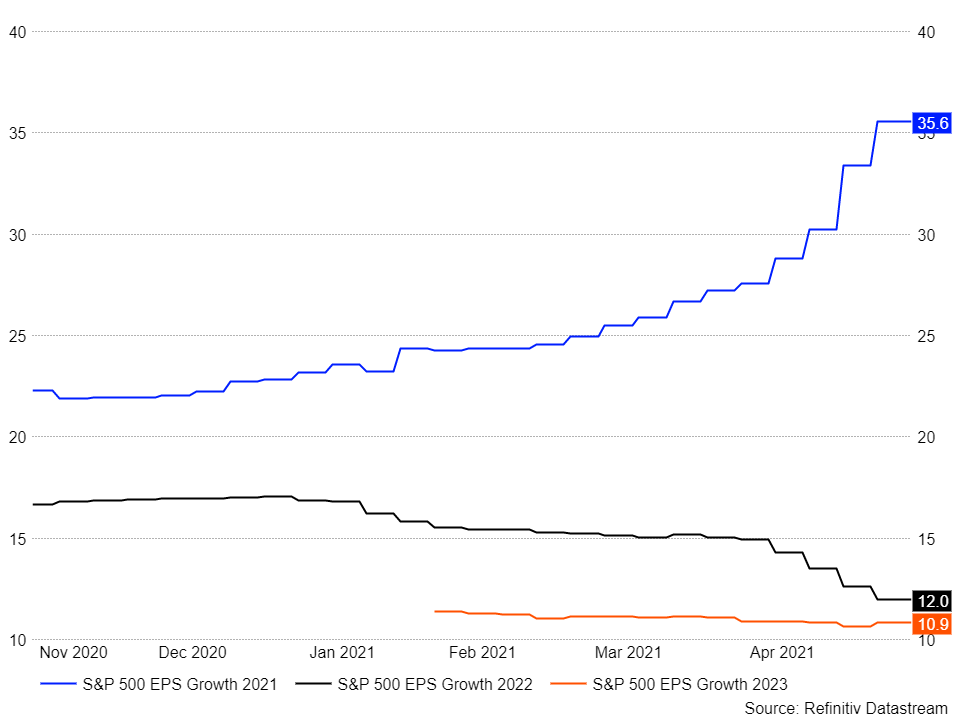

Currently, the S&P 500 is expected to see earnings growth in 2021 of 35.6%, which is then forecast to sink to around 12% in 2022 and 10.9% in 2023. The growth rate for 2022 has been steadily falling since the beginning of April, mostly because estimates for 2021 are rising faster. But there may be more than meets the eye here.

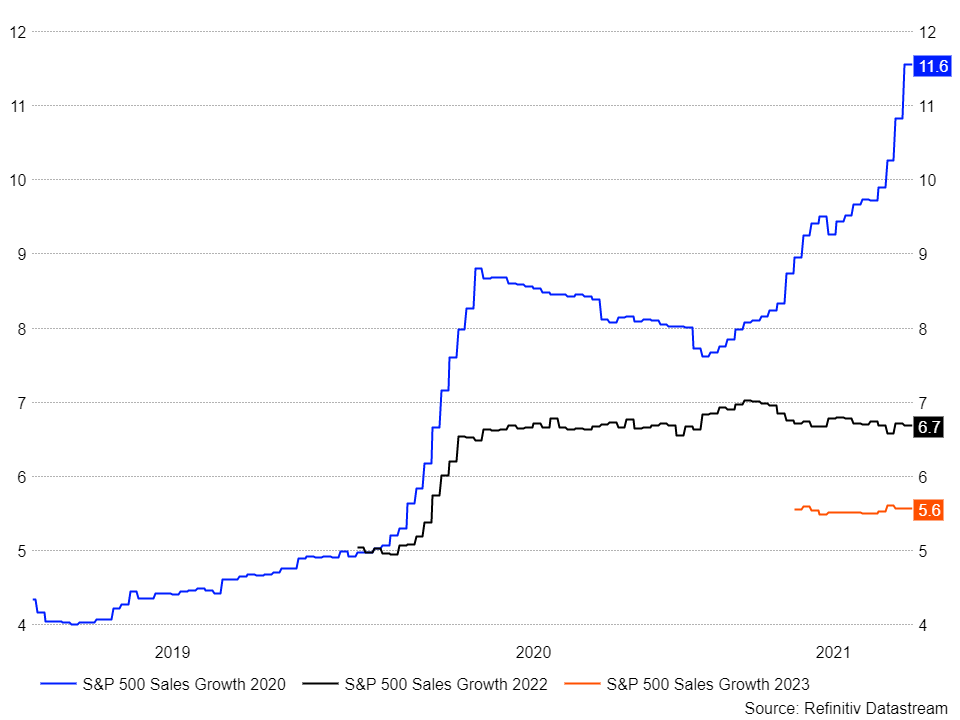

Despite the falling earnings growth rates for next year, growth rates for sales estimates in 2022 and 2023 seem to be trending sideways. Sales growth this year is estimated at 11.6%, 6.7% next year, and 5.6% in 2023.

This could be a reflection that analysts see the economic recovery front end loaded. It may also indicate that earnings growth in 2022 and 2023 will be more negatively impacted by higher input and labor costs—a sign that analysts are now beginning to think about margin compression.

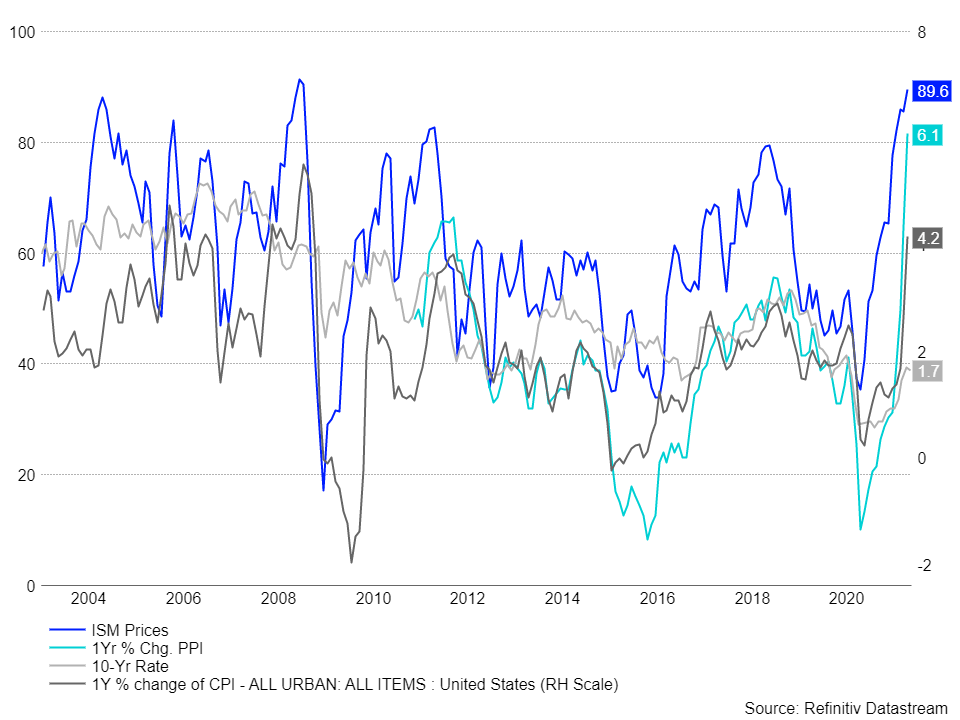

As the CPI and PPI data from earlier this week indicated, inflation rates have certainly been pushing higher. For April, PPI increased by 6.1%, while the CPI rose by 4.2% vs. last year. This was broadly in line with what the ISM data from earlier this month had indicated.

At the same time, the data also seems to suggest that the pace of the economic expansion is slowing to some degree. On May 14, retail sales for April came in below expectations and were flat to March’s levels, showing 0% growth month-over-month. This again was the message that both the ISM manufacturing and service index signaled, with their reading falling slightly from March, suggesting a slowing expansion rate.

The slower pace of economic expansion is perhaps why analysts have been hesitant to increase their sales growth rate in 2022 and 2023, while the higher inflation and wage costs are perhaps taking away from earnings growth in the years ahead. This isn’t to say that earnings won’t grow, but it’s to say there may be some pressure on them in the future.

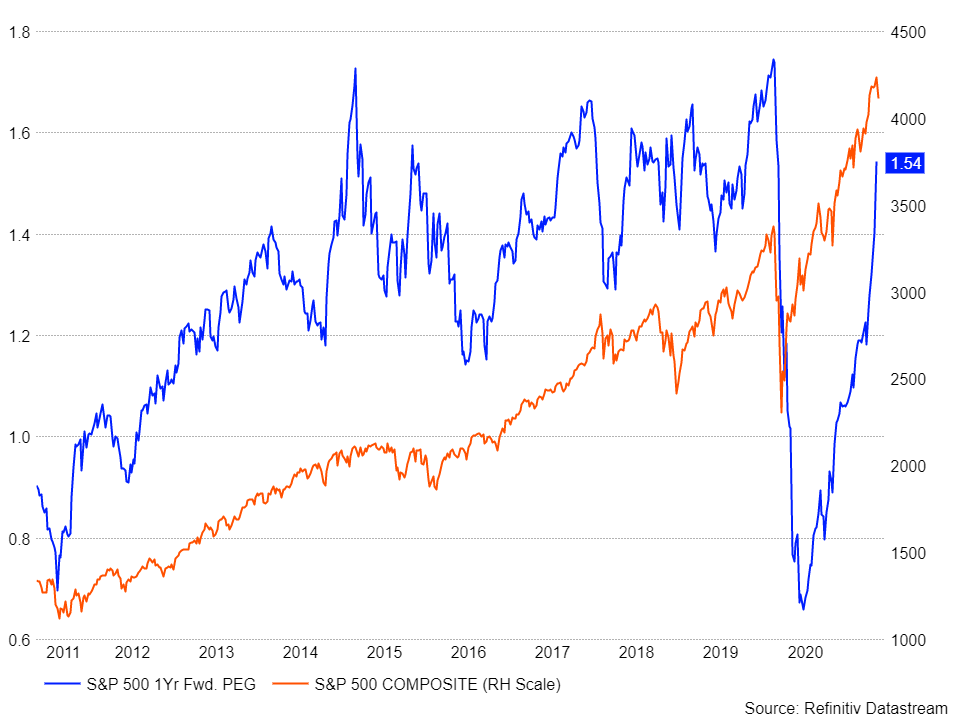

This is likely to present a problem for markets, especially if these growth rates continue to contract. Using growth rates can be an effective way to measure where the PE ratio for a stock or index should be. Based on this one metric, it’s tough to say that the S&P 500 is outlandishly overvalued – one can easily see that as this ratio approaches 1.6, it seems to suggest that valuations are getting stretched.

{kind=link}