My Comments: I survived the crash in 1987, the one in 2000, and was hurt by the crash in 2008-09. The last one because I was older, semi-retired, and without the ability to ride it out until the inevitable recovery.

That we’ll have another crash is inevitable. The huge question is when will it happen and how strong will it be. Since I’m another decade into my retirement, I cannot simply ride it out and hope for the best.

Since I have no idea how old you are, I can only suggest you pay attention and be prepared to move some of your money out of the markets at a moment’s notice. In my judgement, you have about a 30% chance of timing it OK, and a 70% chance of it seriously disrupting your life.

by Mott Capital Mgt. \ 29 APR 21 \ https://tinyurl.com/yjwta2fy

The Fed has been very articulate in the message they are sending, and as I mentioned the last time, they are placating the equity market. But at the same time, daring the bond market to push rates higher. If the Fed gets its wish of higher inflation, it will push long-term rates significantly higher from here, and there is no way for the equity market to combat that.

The problem is that the market already is trading at its most overvalued levels vs. the 10-year since the mid-2000s when all of this low rate policy began. The higher stocks and yields move, the more overvalued the equity market grows, and the more dangerous it becomes.

Higher Yields

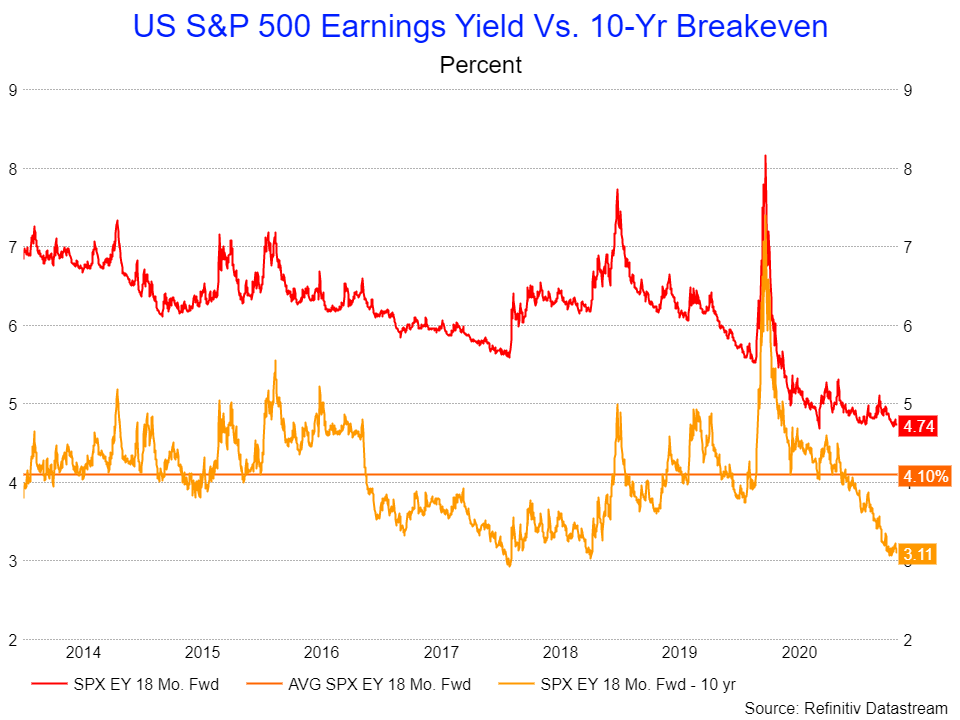

The Fed, in essence, blowing the bond market off is risking a major melt-up in yields, and that will be very damaging to the equity market. The equity risk premium vs. the 10-year yield is now at 3.11%. It means that the earnings yield of the S&P 500 is now trading at its lowest level since January and October 2018. After that, one would have to go back to 2007 to find narrower spreads. That was, of course, before the 2008 recession, before zero interest rate policy, and before massive amounts of quantitative easing were unleashed into the market to keep rates suppressed. Since 2008, this has been the lower bound of this spread.

If rates on the 10-year continue to climb, and the equity market doesn’t correct, the spread will continue to shrink, making the S&P 500 more expensive on a relative basis. A spread of 4.1%, which has been the average since 2014, suggests that earnings yield on the S&P 500 would need to rise to roughly 5.75%, which would equate to the S&P 500 18 months forward PE ratio falling to 17.4, from its current 21.1. While this may seem outlandish, history shows that this reversion to the mean is exactly what has happened over time.

Earnings for the S&P 500 are forecast to climb to $198.29 per share over the next 18 months to $198.29. If it’s the case, then the index over the course of that time could see a rather large drawdown, perhaps to as low as 3,450. That is, of course, dependent on how much rates rise or fall and where earnings estimates go. If rates push above 2% on the 10-year, that earnings multiple for the S&P 500 would need to fall even further, perhaps even as low as 16, which would push the value of the S&P 500 to around 3,200.

Higher Inflation Expectations

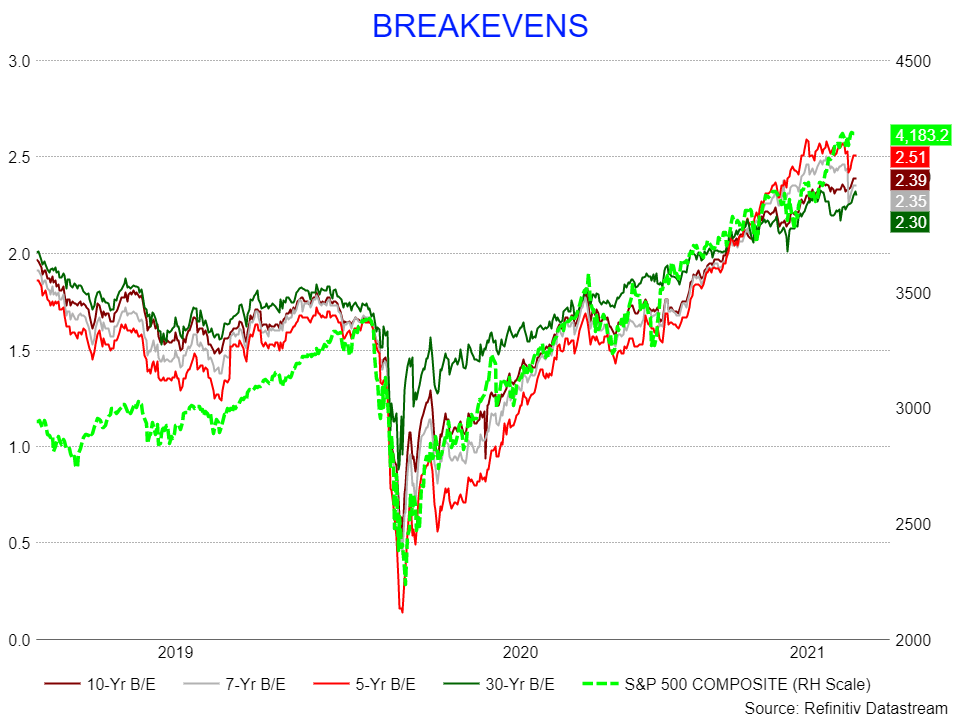

In wanting higher inflation rates, the Fed is essentially forcing the bond markets hand, which means pushing rates to even higher levels. Breakeven inflation expectations are already well above 2%. In fact, the five-year breakeven is at 2.5%. Whether that inflation expectation is real or not is the question because the Fed through QE is likely suppressing TIP rates. Because TIP rates are low and nominal rates are rising, breakeven inflation expectations may be artificially high. Perhaps those expectations would be lower if the Fed reduced its QE program. But perhaps that’s what the Fed wants, to give the illusion of higher inflation to get the future expectations to be higher. Only time will tell.

It seems unlikely that the equity market could stand rates on the 10-year rising to 2% and remain at current prices. It would push the difference between the 10-year and S&P 500 earnings yield 40 bps points lower, to around 2.7%. It also would send breakeven inflation expectations toward 3%, assuming no changes. This would send the equity market into a hazardous zone.

More Attractive Vs. The Dividend Yield

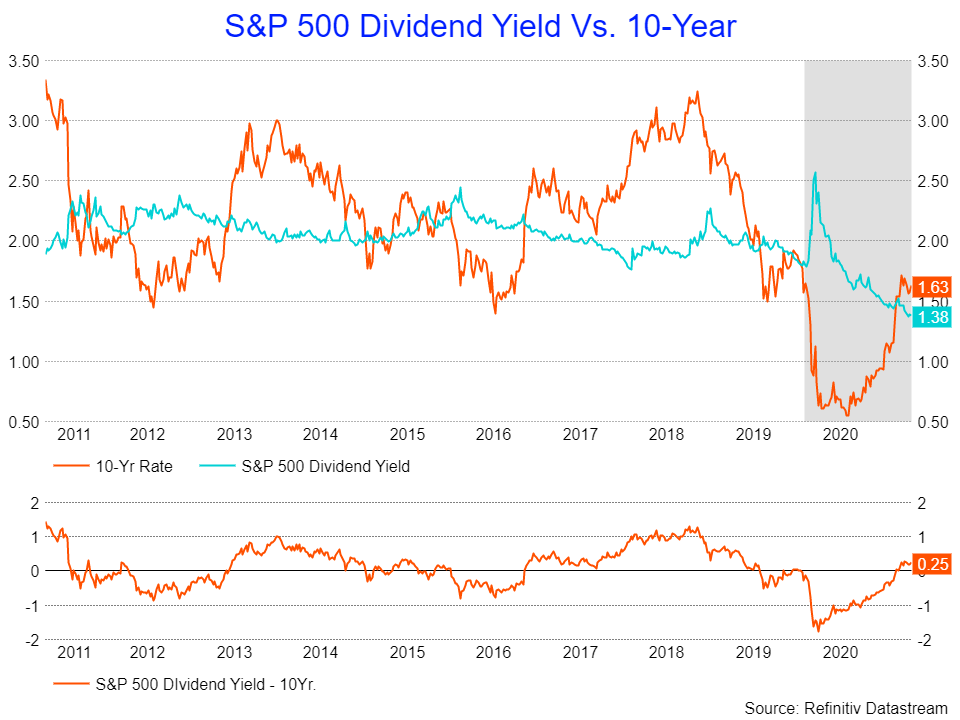

Additionally, the dividend yield on the S&P 500 now at 1.38%, the 10-year rate has a 25 bps premium. A further 40 bps rise in the 10-year would push that spread to around 65 bps, and while it isn’t at the high end of the range, it makes the 10-year more attractive and likely weighs on the multiple of the index as well.

The Fed may very well push the narrative. It isn’t the time to talk about tapering. However, in wanting higher inflation, the Fed also is sending long-end yields higher as well. While it sounds all fine and great for the equity market now, it won’t be if rates get just a little bit higher. Powell clearly made the correct call at the March meeting, buying himself another six weeks, but with a slew of economic data coming in the next few days that will show a lot of inflation, he may find the next six weeks harder to endure.

Reading The Markets is designed to provide members with a better understanding of the stock market and to provide stock ideas. Just like the free articles you have grown to love reading.

Or if you want to learn about how the markets function, I can teach you that too.