My Comments: Following the market crash last March, and the relatively unsustainable surge upward over the intervening months, it’s my belief that sooner rather than later, we’ll have another crash.

Too many people believe the economy is doing great, and are expecting stock market valuations to keep rising forever. They also have a hard time separating economic viability with stock market performance. Yes, there’s a correlation, but it’s far from 100%.

So my question going forward, is where am I likely to see my money grow as the world emerges from the pandemic and the Biden/Harris administration changes the national dynamic in the coming years? I think VHT has significant potential.

by Dean Young \ 17 Nov 2020 \ https://tinyurl.com/y6ndp8dx

Summary:

* VHT is a low cost ETF that provides exposure to healthcare sector, primarily pharmaceuticals, medical equipment, and insurance.

* VHT’s exposure to well-established companies with stable market products makes it defensive in this economic environment.

* VHT is also poised for growth as the economy recovers and healthcare spending continues to skyrocket.

The Vanguard Health Care ETF (VHT) is a diversified low cost and passively managed ETF that tracks the MSCI US IMI Health Care 25/50 Index. True to Vanguard’s reputation for low cost indexing, VHT’s expense ratio is a rock bottom 0.10% and gives you access to over 400 U.S. based healthcare sector holdings.

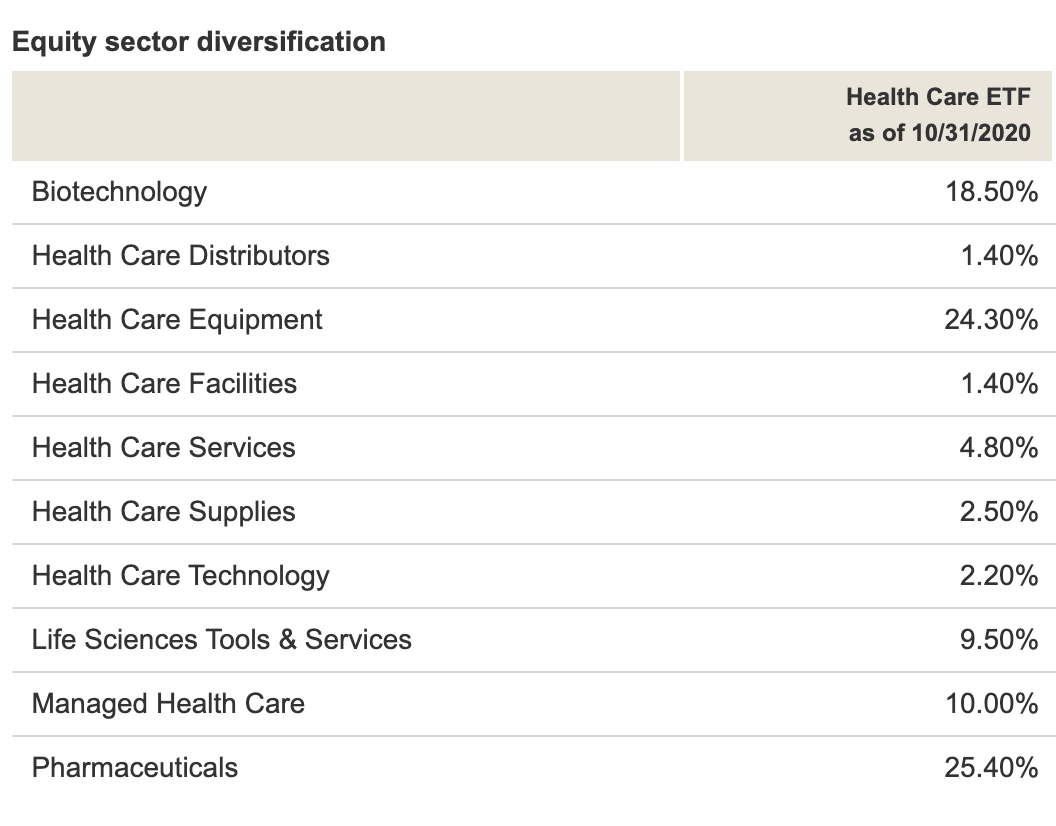

Holdings

VHT is fairly diversified across several areas within healthcare but tends to be more concentrated in physical products such as pharmaceuticals, biotechnology, and medical devices/equipment rather than in services and facilities (hospitals and nursing homes). VHT also has moderate exposure to “Managed Health Care” which is basically the health insurance industry and its healthcare network.

Source: Vanguard

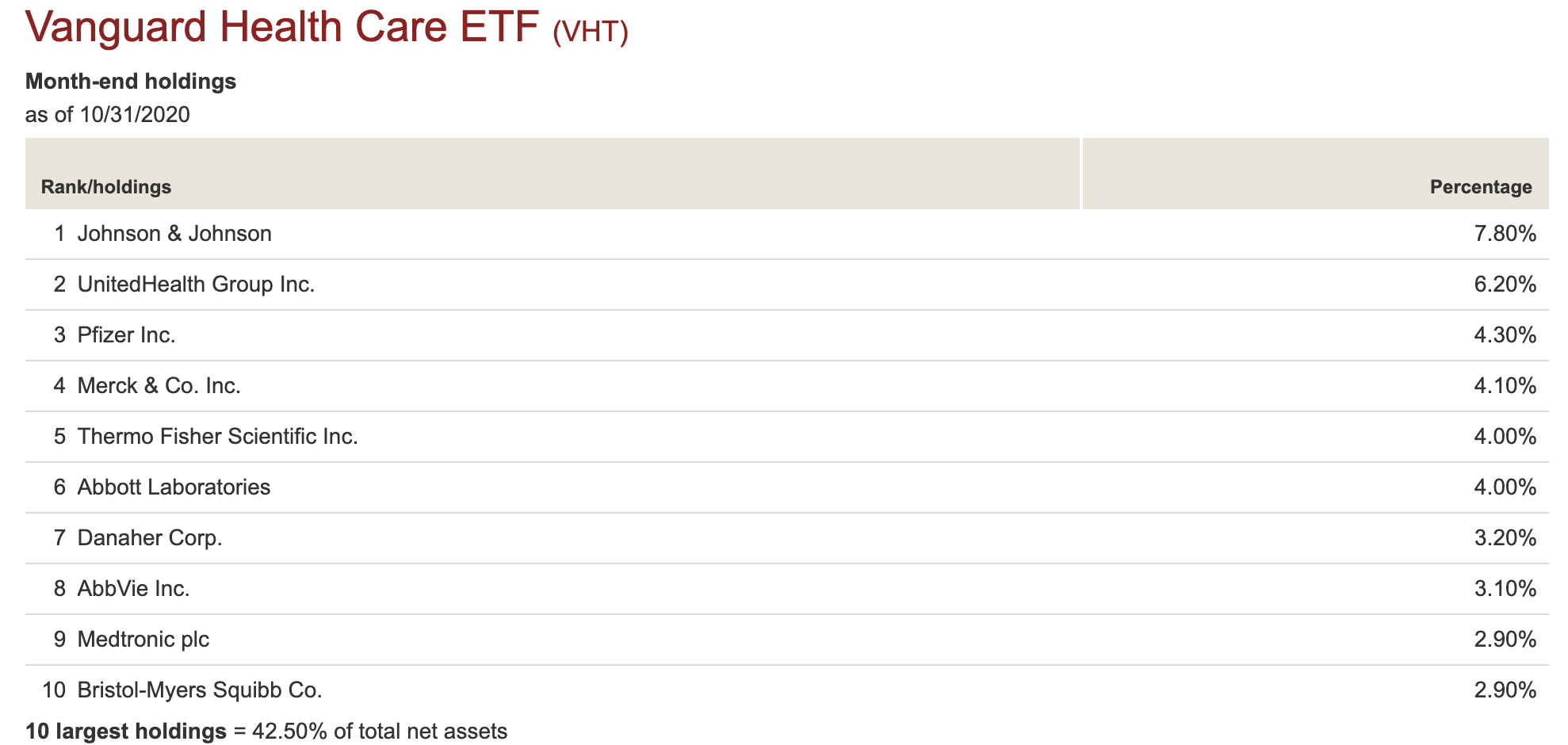

While VHT does diversify across market caps, it heavily leans towards well-known large cap pharmaceutical, equipment, and biotech names. The median market cap for VHT’s holdings is $76B. VHT is also heavily weighted towards its top ten holdings which currently account for 42.5% of its assets.

The names in the top ten are typically the biggest players in their industries. The largest holding is Johnson & Johnson (JNJ) which is incredibly well diversified across consumer staples as well as pharmaceuticals (including a COVID-19 vaccine candidate). The second largest holding is United Health Group (UNH) which is the largest healthcare company in the world and primarily operates in the insurance industry.

Pfizer (PFE), Merck (MRK), Abbott (ABT), AbbVie (ABBV), and Bristol-Myers Squibb (BMY) focus on pharmaceutical drugs across a wide spectrum of diseases and conditions. Thermo Fisher Scientific (TMO), Danaher (DHR), and Medtronic (MDT) focus on developing and manufacturing medical devices, lab tests, and equipment for severe and chronic diseases.

Source: Vanguard

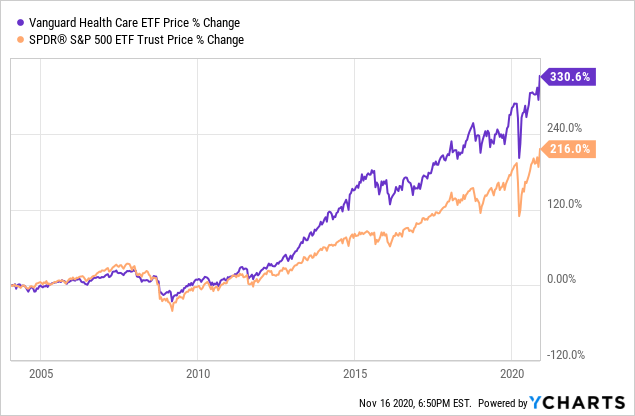

Historical Performance

VHT’s total return performance has crushed the S&P 500 over the past decade. It also recovered much more quickly in the recent COVID-19 market crash.

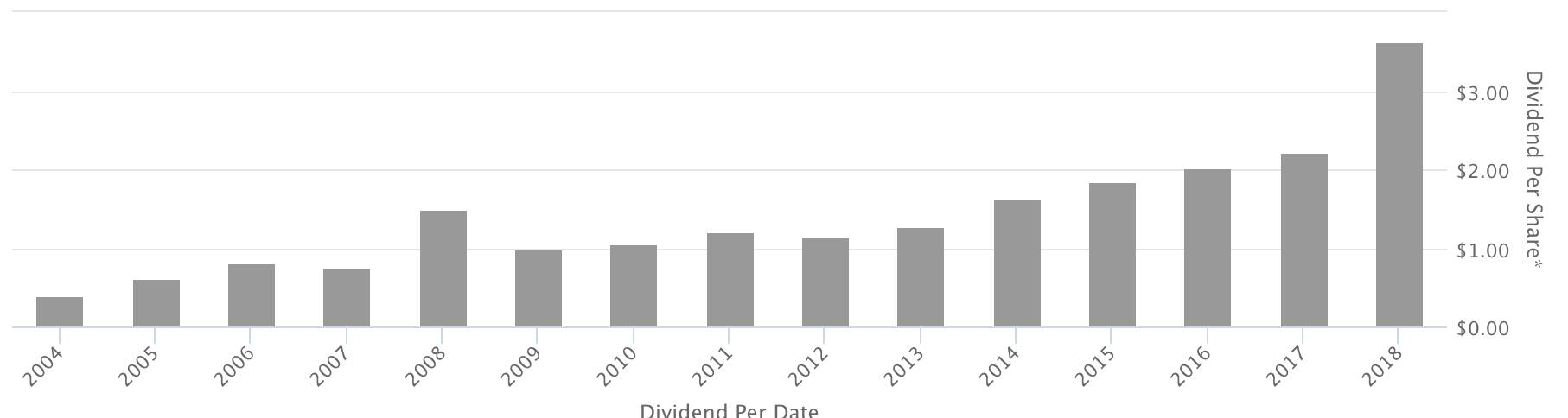

VHT also pays a growing dividend, currently yielding about 1.5% which is in line with the S&P 500.

VHT Dividend Per Share Growth (Source: SeekingAlpha)

Defensive

The COVID-19 pandemic has created a huge drop in elective surgeries at hospitals to make capacity for COVID patients and this trend is likely to continue. Hospitals typically create the most profit from elective surgeries and thus are hurt significantly by this trend. Luckily, VHT is not heavily exposed to healthcare services and hospitals and will be shielded from this effect.

Instead, VHT holds a lot of pharmaceutical and medical equipment/device companies that produce “essential” medical products. The demand for these products will not be harmed by any potential lockdowns or rise in COVID cases. Additionally, VHT’s health insurance companies also benefit during the pandemic as their customers are likely staying out of hospitals unless absolutely necessary (for both safety and capacity reasons). As of October 2020, non-COVID hospital admissions are still well below normal. This reduces costs to their insurance companies, while they or their employers continue to pay premiums.

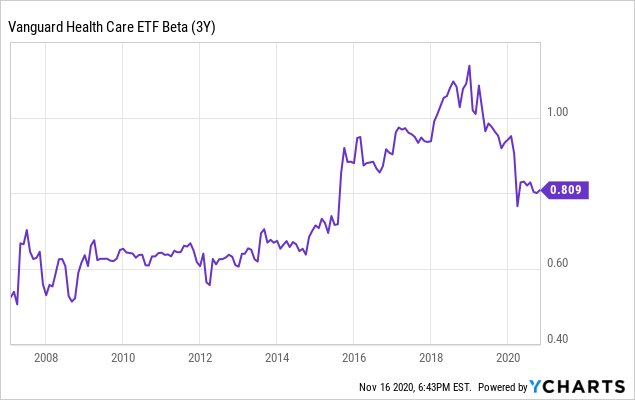

VHT also has had generally lower volatility than the S&P 500 as measured by 3Y Beta, with the only recent spike above 1.0 driven by interest rates rising in late 2018. This can seem counter-intuitive for a pharmaceutical heavy index but the top holdings of VHT are large companies with a long history of established FDA approved products with predictable costs, revenues, and profits. These companies don’t face the same volatility as smaller pharmaceutical companies that rise or fall by double digits on sudden news about their few products in the pipeline.

Growth Prospects

VHT also has potential for modest growth when the economy recovers from the pandemic. Two of the top ten holdings, PFE and JNJ both are producing COVID-19 vaccines, the former of which was the first to announce a 90%+ effective vaccine. PFE has already seen a jump in share price and JNJ could soon follow. Once the pandemic is under control, pent-up demand for elective healthcare services could spur more growth for the products generated by companies in VHT.

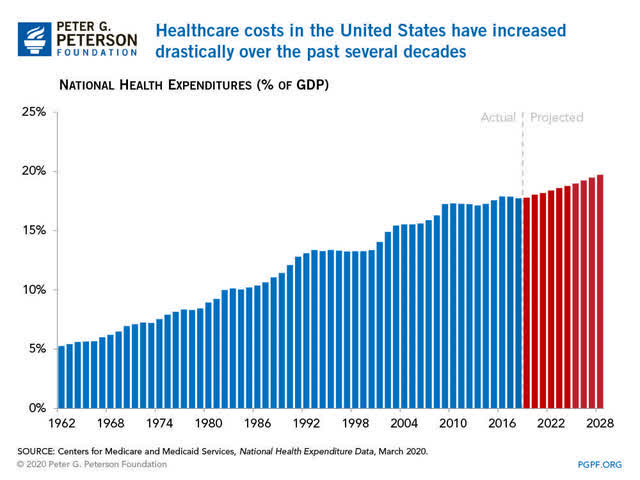

Most importantly, regardless of the pandemic, there has been a continual explosion in healthcare spending in the U.S. The U.S. is projected to spend over $4T on healthcare in 2020. As a percent of GDP, healthcare spending is projected to continue to grow to nearly one-fifth of GDP by 2030. This is a huge market that VHT’s companies will continue to capture. An investor can’t do much wrong investing in an industry that takes up 20% of an entire country’s spending.

Source: Peter G. Peterson Foundation

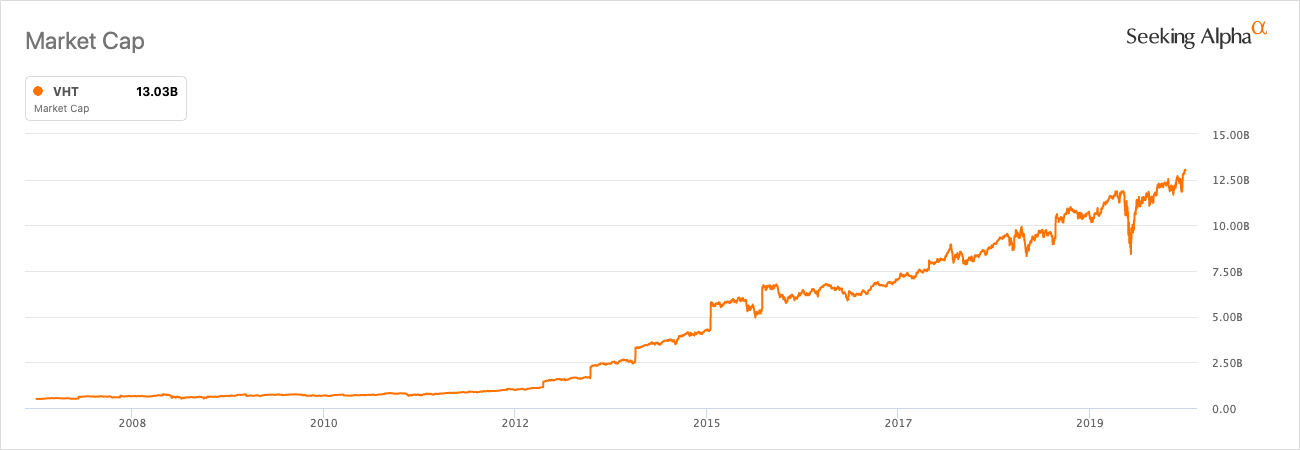

The market cap of VHT has expanded similarly, growing from under $1B in 2008 to more than $12B in 2020, following the trend of increased healthcare spending.

Valuation

The average P/E ratio of VHT currently sits at about 24x. Compared to the general market as measured by the S&P 500 with P/E ratio at about 36x, VHT seems very reasonably valued. Investors are paying about 33% less per dollar of earnings for VHT for a fairly safe healthcare sector during the pandemic recession while still having significant growth prospects.

Risks

While there is not yet widespread political support for Medicare For All, should it become a reality, it would transform the U.S. health insurance industry into a single-payer system run by the government and funded through taxes. It would eliminate or significantly reduce the role of private insurance. There is some evidence that Medicare is able to reduce health costs with better bargaining power over that of private insurance.

If Medicare For All becomes the only payer, it would have significant leverage in negotiating drug prices as pharmaceuticals and medical equipment companies would be forced to accept whatever payment offered. Additionally, health insurance companies could potentially be squeezed out of business and reduced to only managing claims and networks for the government. These changes would significantly impact the profitability of the healthcare sector.

There is no immediate risk to VHT as the current Trump administration and upcoming Biden administration have no plans to introduce Medicare For All. However, investors in VHT will always be exposed to volatility when the market prices in news of a bill being introduced. A recent example is when Medicare For All discussions began heating up in 2019, causing a slide in health care stocks, only to rebound when Elizabeth Warren said she would not pursue the policy immediately if she became president.

Conclusion

VHT is a solid healthcare play during the pandemic and comes with good recovery and growth prospects post-pandemic along with a fair valuation. There are minimal business risks as most of the companies in VHT provide essential medical products. The only major risk is Medicare For All being introduced but it is not likely to come any time soon as it is not favorable politically. It’s never too late or too early to invest in such a solid ETF like VHT.