One of the existential threats faced by all senior citizens is developing the need for Long Term Care or LTC. It’s when you can no longer perform some of what are referred to as Activities of Daily Living or ADLs. It means there’s a need for help from someone else when it comes to things like preparing food, or bathing, or taking your meds. It typically surfaces toward the end of one’s life, has the potential to cost an enormous amount of money, not to mention the personal need to accept the inevitable.

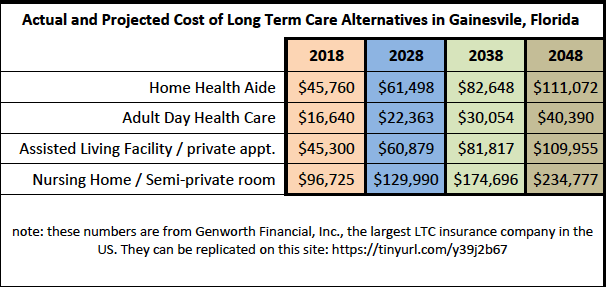

I live in Gainesville, Florida and this is a chart I prepared some months ago to appear in my online school, Successful Retirement Secrets.

As a long time professional in the world of financial planning, I’ve raised this issue with clients and from time to time, helped them find a partial financial solution. My choice has been to encourage solutions that leverage the money spent such that if the existential risk becomes reality, there are many more dollars available than what was spent. At the same time, if no LTC need arose, those same leveraged dollars would pass to a beneficiary.

Over the years, some clients chose to purchase insurance policies that for a monthly premium, would provide benefits if qualifying circumstances happened. This is not unlike the car insurance most of us buy. If no claim is made, our premium dollars stay in the hands of the insurance company and are used to pay the claims of others. No accident, no benefits paid.

The dilemma those folks are now facing is that insurance companies grossly underpriced those policies. In a competitive world, they simply didn’t charge enough money for the coverage offered and are now presenting their customers with significant price increases. Few of them ever expected so many people to live as long as they do today.

Many of the companies in this business 25 years ago are long gone. The ones that remain survive by demanding higher premiums. If customers declare they cannot pay more, the company drops their coverage, no longer has to pay benefits, and gets to keep the premiums paid to that point in time. It may result in bad publicity, but their motive is to stay in business, make a profit, and be able to legitimately pay benefits under the terms of the original policies sold to customers who agree to pay the higher premiums. Imagine if your car insurance premiums started increasing 25% every year, would you still own a car?

My favored approach, as referenced above, was to use policies built on a life insurance platform. These contracts are issued as a life insurance policy with provisions that allow someone who incurs approved LTC costs to receive an advance on the death benefit. Depending on the age when purchased and existing health issues at the time, $1 spent might result in $4 to pay for LTC.

They come in several distinct policy variants with different mechanisms for paying LTC benefits. The only downside is they are purchased with current dollars that might not reflect the inflated cost of the LTC benefit when a need arises. This is true of most life insurance policies because a typical $100,000 death benefit policy today will not have the purchasing power of $100,000 down the road if there’s inflation over that time period. The upside is that you haven’t died until then.

Here’s a chart from a prominent life insurance company that today offers contracts to potential buyers of a life insurance policy. The policy has a built in ability to use death benefit dollars before you die. It shows approximate costs of alternative LTC solutions today and how those costs are likely to increase. There’s also a fairly significant difference in costs depending on where you live.

Simply stated, getting old can be a royal pain in the ‘you know what’, or it can be a marvelous outcome. I’m just glad my time has not yet arrived.

Tony Kendzior \ November 15, 2019